A Microcap Stock with Explosive 2026 Potential

Early Access Video for Paid Members

Investing in upward-cycles is one of the best ways to make money in microcap stocks.

Investing on downward-cycles is one of the easiest ways to lose money.

When I get a clear upward-cycle in a stock I know well - I get excited.

Today I’m seeing an upward-cycle in a stock I know well.

Sabio Holdings (TSXV: SBIO - OTCQB: SABOF)

Quick Thesis

Sabio Holdings is a growing ad-tech specialist in streaming television (CTV/OTT). While Sabio has a growing core business of diversified advertising revenue (37% CAGR), due to the high quality of their data being able to deliver ads to niche audiences - Sabio sees a spike in revenue and margins during election years in the United States (86% CAGR). 2025 is NOT an election year - resulting in share price dropping 52% from 52-week highs. However, the upcoming 2026 US midterm elections are expected to set records for spending, with budgets projected to hit ~$10 billion with ~$2.5 billion expected to be spent on CTV ads. Add in a significant number of mayoral elections to this mix, and Sabio in 2026 could see significant upside in both EPS and operating cash.

Need more good news? The 2026 elections won’t necessarily just be crammed into a one-quarter spike in revenue. Due to the number and diversity of elections there could be an increase in revenue starting in early 2026 and ending late in 2026.

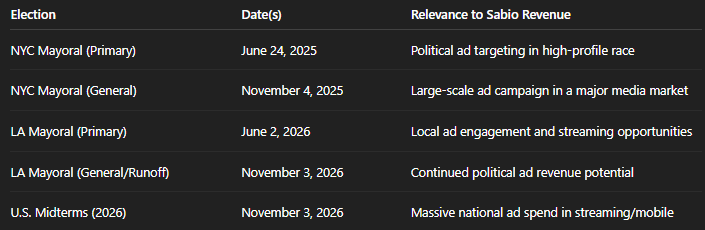

Elections to Watch (2026)

U.S. Midterm Elections – November 3, 2026: All 435 House seats, 35 Senate seats, and 39 Governor races.

Key swing states & battlegrounds: e.g., Michigan, Ohio, Florida—top ad spend states (e.g., Michigan alone projected for nearly US $936 million)

LA Mayoral race (primary) June 2nd, 2026 and Sabio is a California headquartered company (this is their back yard).

Need even more good news?

Potential legal watershed: A pending Supreme Court decision on party-candidate coordination rules could allow unlimited ad buys by parties, potentially dramatically expanding ad spend volume (especially for streaming TV). A ruling is expected sometime in early 2026 in anticipation of the US midterms.

Some Basic Numbers to Start

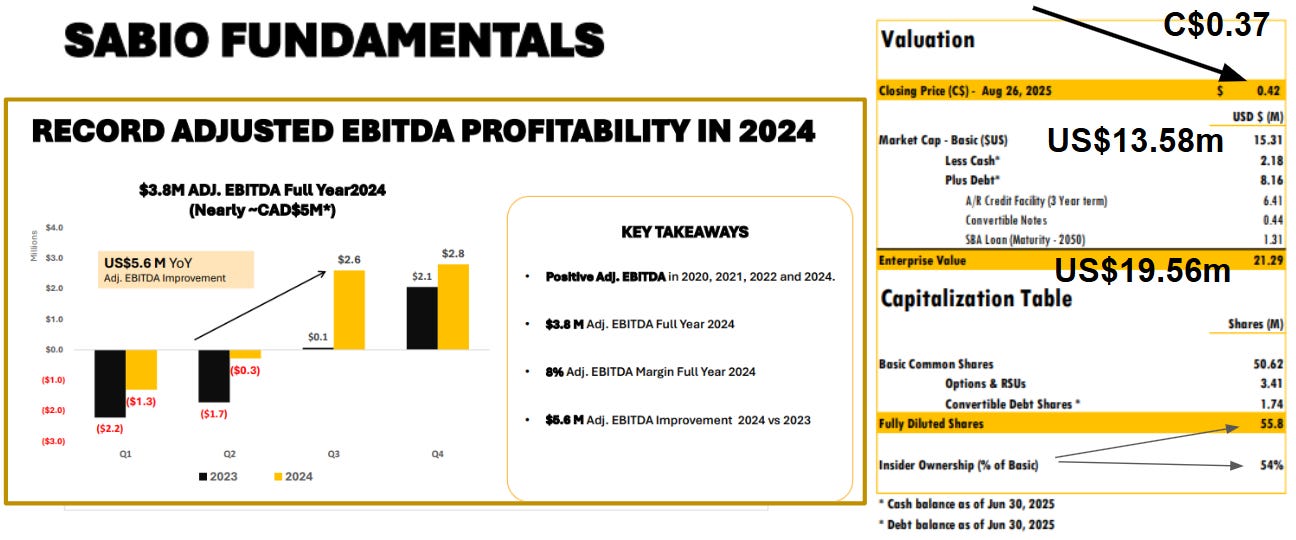

So the potential here for a VERY successful 2026 for Sabio looks attractive. Please run your own math, but here at a share price of $0.37 CAD I get a USD market cap of $13.58M and a USD Enterprise Value of $19.56M. In 2024 they increased their adjusted EBITDA by $5.6M to a positive $3.8M and if they can do that again in 2026 that gives them an EV/adjustedEBITDA of 5.15x for a high growth company - and with potential they outperform their 2024 numbers.

What’s even more interesting is that Sabio Holdings hasn’t been prioritizing profitability. At their most recent earnings call an analyst asked the question of when shareholders can expect some operating leverage and more consistent profitability, and the answer I heard was once they closer to $100M in revenue - they have a long way to go.

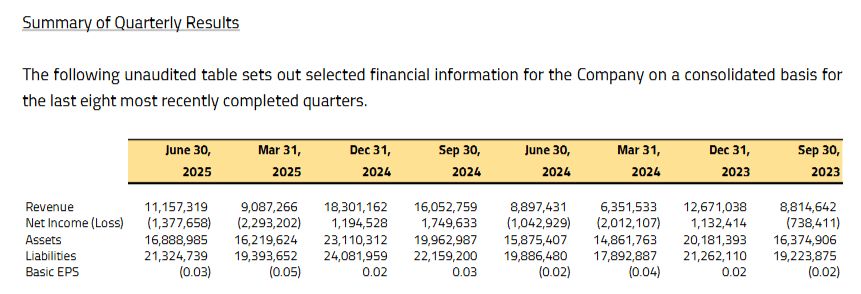

However when you look at the opportunity in front of Sabio in 2026, it’s hard to ignore that even without consistent profitability from year to year there is opportunity here. Investors see these cycles and choose to sell their shares of Sabio before the drop into the “non-political revenue years” and I understand that. Not only the opportunity cost with that money, but it’s also hard to watch a company go from unprofitable to profitable and then unprofitable again. But the core business is improving even in the challenging years. Looking at the below table Sabio reported ~$15M of revenue in the first 6 months of 2024 and have now reported ~$20M in the same 6 months in 2025. It just cost them more more to get there.

High top line growth, with a reckless inconsistent bottom line earnings. That’s the story right now that Sabio needs to change.

And that’s the risk 👆

Before I move on to the risks, I will leave you with some words from Sabio’s CFO Sajid Premji during their Q2-2025 earnings call that potentially highlights the opportunity in the next 12 months.

This is the challenging year (2025), but I think it's what we are confident in is that the moves we're making today are gonna pay off in a big way next year and thereafterwards. Now we're gonna see an expansion of EBITDA margins next year. So I think that in 2024, we saw 8% EBITDA margins. I don’t see why we can’t match that or exceed that in 2026. We're gonna see even stronger top line growth across our core business and also growth in our political apparatus too. So the moves we're making today are gonna pay off in a big way.

Every Stock has RISK - Sabio has Significant Risk!

As always I say for microcap stocks for every bullish indicator there is usually an equally compelling bearish indicator. I always say that’s what sets me apart from other microcap stock platforms is I LOVE discussing the risks of these companies. A quote I believe in is “A team is only as good as its weakest player” well I think that applies to stocks where a company is only as good as it’s greatest risk. There’s not much point buying a stock with 50% upside if there’s significant risk of 100% loss.

What are some of the risks of Sabio Holdings?

❌ Political advertising revenue captured by Sabio is uncertain.

While true estimates vary, a quick Google search is telling me there was $14.8 billion spent in the 2024 US elections. Sabio Holdings reported $7.5M of political revenue in 2024 - that’s about 0.05% of the total dollars spent. A VERY small amount! Sabio says they are more prepared this time around for 2026 elections, and I wonder if they can capture $15M of revenue. I have to admit I was expecting more than $7.5M of political revenue in 2024, they definitely did not meet my expectations. Am I expecting too much of Sabio in 2026?

❌ Operating Losses are Adding Up 📈

Q2 2025 still saw Sabio report an adjusted EBITDA loss of ~$1.2M despite revenue gains. I previously mentioned revenue has ramped up in 2025 from $15M to $20M despite the lack of political revenue. However “spending for growth” has been eroding margins and increasing EPS losses. Shareholders have to wonder - is the lack of consistent profitability due to quickly growing expenses is a good strategy - or is it hiding a failing business model?

❌ Expenses are Escalating Quickly 📈

Spending for growth is very popular in 2025 for many companies - it’s addictive. It also adds significant risk! If growth does not come then that money was wasted, and many microcap stocks do not have money to waste. Sabio is basically out of cash and has been spending on cloud infrastructure, marketing, and hiring sales staff in the expectation of high growth. However if they don’t get growth in their cash production - then what? Dilutive financing? High risk notes? Sabio is a “boom or bust” stock right now in my humble opinion.

❌ Cash and Cash Flow 💵

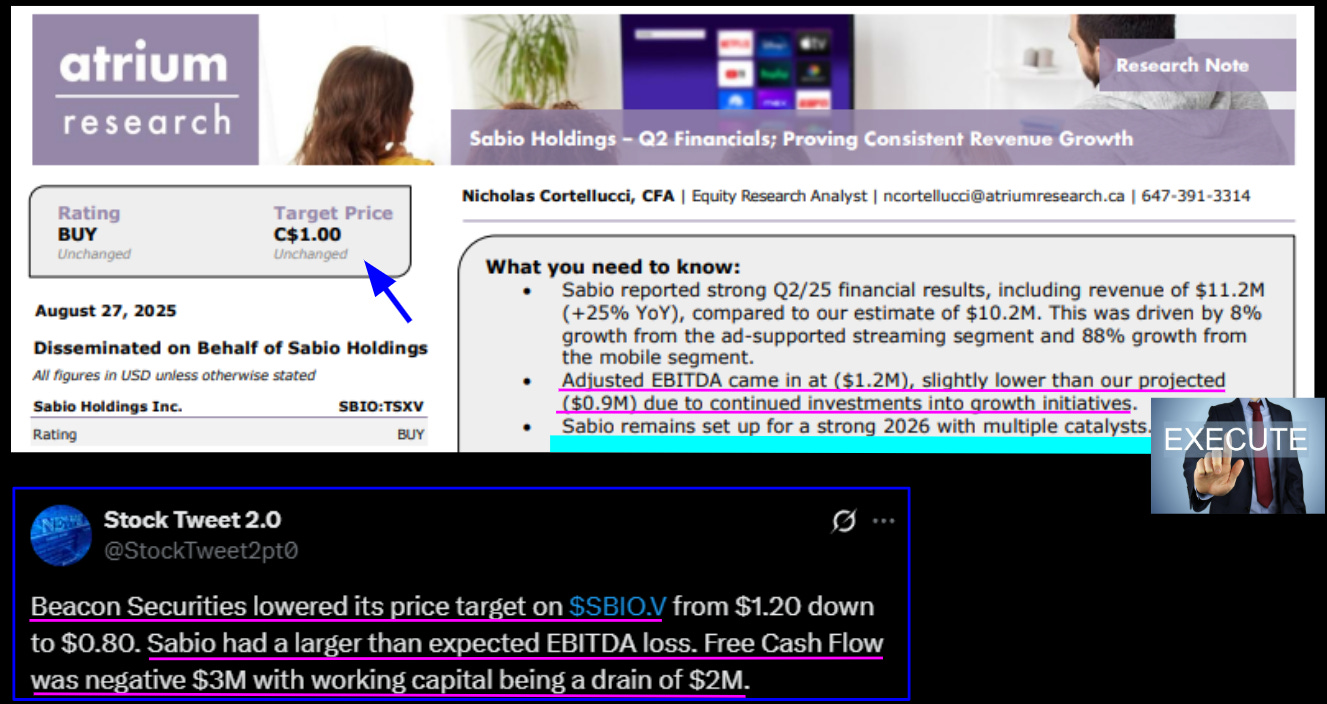

Ultimately I believe most “RISKs” are just the noise around CASH. If Sabio captures ~$15M of higher margin political revenue in 2026 I would expect them to be strongly cash positive - but that cash may only begin to offset their current losses in 2025. Then what? The risk here with Sabio is that they simply run out of cash and need a highly dilutive financing at a low share price. Beacon Securities reduced their price target on Sabio, crushing it down from C$1.20 to C$0.80 specifically noting free cash flow losses. It’s a problem.

👆This slide here says so much! Atrium Research points outs Sabio’s higher than expected top line revenue growth, while Beacon Securities points out Sabio’s higher than expected bottom line losses. Atrium Research points out the multiple potential 2026 catalysts, but of course I have to point out catalysts only occur through execution.

Summary of Risk

I don’t think the risks for Sabio shareholders are independent issues, it’s not one thing that can be “fixed” but a connection of issues.

Is their core business truly a profitable and successful model, or not?

If their core business is a working business model then over time their operating leverage kicking in should result in a profitable and growing company with an improving balance sheet.

If their core business isn’t a working business model then an already ugly balance sheet at some point becomes unmanageable.

The risk is that we don’t know yet.

During perfect conditions during US elections Sabio gives hints they could become that profitable growing company.

During more challenging conditions we see high risk notes funding a company that’s nearly out of cash.

What do you think is the truth here?

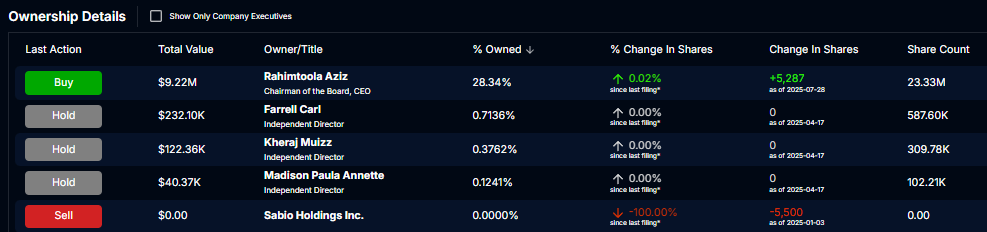

Insider Ownership is Impressive

Significant risk! And Sabio’s share price has dropped significantly on these risks. However, I do need to give a shout-out here to Sabio’s CEO Rahimtoola Aziz. Sabio is a founder led company with their CEO owning significant chunk of shares, with Sabio saying they have 54% insider ownership in total. So when share price drops 52% it’s not just the average retail shareholder who feels that drop.

My Thought Process

I always compare investing in microcap stocks to a game of Texas Hold’em Poker. Balancing probable outcomes as you get more information through your hand, the flop, the turn, and the river. With the stock market being the “table” and the players you are competing against. Some people go all-in before the flop, while other people only play one hand in twenty. There are different ways to win.

I like the hand Sabio is giving me.

There is evidence from 2023 to the 2024 election year that they can produce positive growth in good conditions, and share price was rewarded for it. Can they repeat these results? 2026 looks like a clear upward cycle for Sabio Holdings with growth in their core business getting a potentially large boost from the political revenue they get every two years. It’s a pretty simple bull thesis to get high growth and improved earnings in near perfect conditions.

However the risks are also real. Too many times I have watched companies say for years “we are spending for growth” when really they are simply making excuses for a poor business model. This usually gets exposed when the growth stops, and the weak balance sheet leads to immediate dilutive event or debt on terrible terms. Not a good place to be for shareholders.

The good news for investors looking at Sabio is that (like a good hand of poker) you don’t really have to make any quick decisions. Share price is arguably “cheap” right now and some people may want to risk a bet pre-flop. However if the bull case for Sabio comes true then we should see improvement in Q3 (the turn card) and Q4 (the river card) and this should give investors more information to make informed bets decisions.

Summary & Videos

A high potential reward for Sabio shareholders if they execute.

A high risk of losses if they fail to execute.

A (microcap) stock market story as old as time.

My expectations for Sabio Holdings are very simple:

Produce cash and improve the balance sheet.

I previously bought shares of Sabio Holdings at roughly $0.25 CAD and then sold above $0.55 CAD. Definitely NOT financial advice, but as discussed below in my disclaimer I have decided to give Sabio another chance. I purchased a small starter sized position in Sabio Holdings with the expectation to buy more shares if they show execution through Q3 and Q4. I have no plans on selling my shares, however as always I absolutely 100% will trim or sell if conditions change or they fail to execute as per my expectations.

In addition to my video I would suggest anyone interested in Sabio Holdings also listen to their most recent earnings call for Q2 of 2025.

If Sabio reads this article the one thing I would like to say:

Your balance sheet is scaring investors away. If 2026 is profitable I want to hear how 2027 is going to be profitable. I love the growth, but at some point Sabio needs enough profitability to self-finance to avoid the high risk debt that drives share price down 52%. And YES, even if that means a little slower growth. I know your argument about the huge market opportunity and how you are investing in cycles, but eventually if shareholders keep taking 52% losses in their portfolio you won’t have many shareholders left, and few investors willing to take the risk to believe in you. The microcap community isn’t very large and I speak to investors all day - I already see less people interested in Sabio today than when I first introduced you two years ago. Food for thought.

Seriously, this is NOT financial advice.

I mean it. None of this is financial advice—I say it all the time, and I genuinely mean it. I don’t know you. I don’t know your experience level, risk tolerance, debt situation, or anything else about your financial position. So please, don’t buy, sell, or hold a stock just because of my opinion in this article.

I’ve been wrong plenty of times, and I strongly encourage everyone to invest within their own capabilities and consult a financial advisor if needed.

I started a 4% position in my microcap portfolio on Sabio Holdings stock on the TSX Venture exchange ($SBIO.V) at ~$0.40 CAD. I own no other assets of Sabio Holdings and do not receive compensation (of any kind) from any company that I provide coverage for including Sabio Holdings.

Thank you! 🙏