Another 5 Stocks for Planet MicroCap Vegas

Free Article

My first Planet MicroCap Vegas article covered five companies that I think deserve investor attention.

Link to my top 5 stocks for Planet Microcap Vegas article here.

This article is the next layer down the research funnel.

These are not necessarily my “best five” remaining ideas. They are five more companies I want to understand better in Vegas because each one has something interesting going on: profitability, operating leverage, turnaround potential, misunderstood growth, or a possible inflection point.

As always, this is not financial advice. This article is for informational and educational purposes only. These are short introductions, not full research reports. Microcaps are risky, illiquid, and often humbling. Verify everything against filings, financial statements, and your own due diligence.

Jerash Holdings (NASDAQ: JRSH)

Market Cap: ~$44M

Q3 FY2026 Revenue: $41.8M, +18% YoY

Q3 FY2026 Gross Margin: ~17%

Q3 FY2026 Net Income: ~$1.2M

9M FY2026 Revenue: $123.4M, +6% YoY

9M FY2026 Gross Profit: $19.4M, +14% YoY

9M FY2026 Net Income: $2.0M vs. loss of $0.7M last year

Q4 FY2026 Revenue Outlook: +23% to +26% YoY

Jerash manufactures custom sportswear and outerwear for major global apparel customers. This is not a glamorous business. It is apparel manufacturing: low-margin, customer-driven, working-capital intensive, and exposed to freight, tariffs, labor, customer concentration, and geopolitical perception. That is also why it is interesting, most of the macroeconomic factors right now are tailwinds for Jerash.

I explain this more in the following video:

A one-hour deep introduction to Jerash Holdings (NSDQ: JRSH) on YouTube.

Macroeconomic momentum seems to be gaining for Jerash. Trump and the trade war has created chaos for clothing manufacturers as countries have been threatened with higher tariffs, in some cases high enough to be considered a trading ban. Companies have been looking for stable and safe places to diversify their manufacturing.

Most of these companies are diversifying away from Asia, and unfortunately for Trump they probably won’t be expanding into the very expensive US labor market. Jordan has a cheap stable labor force, low tariffs, a business friendly government, and really isn’t an important enough country for anyone to threaten or intentionally harm. If I were a large clothing company I wouldn’t bet 100% of my business on Jerash, but it does offer some attractive low-risk diversity.

This momentum can be seen in the nine-month numbers. Q1 was weak with negative growth of 3%. Which then recovered in Q2 with 4% growth. Meaning Jerash was basically flat with no growth for the first half of the year.

However, the promised ramp-up showed up in Q3 with 18% growth, and guidance for Q4 is even more impressive at 23-26%. Jerash could potentially move from ~0% growth in H1 to ~20% growth in H2. And that should be enough to get investors a little more interested in what 2027 could look like.

Potential Rewards: Momentum looks good for Jerash to achieve the “twin engines” of a potential share price increase - earnings growth and multiple expansion.

Earnings growth: 18% growth in Q3 and management has guided Q4 revenue to increase 23% to 26% year-over-year, with a gross margin target of 14% to 16%. If the company delivers even the low end of that revenue growth while keeping margins stable, FY2026 should show clear operating progress with recent investments in capacity. Creating an attractive setup for even more growth momentum in 2027.

Multiple Expansion: I am hoping for some multiple expansion through discovery from microcap investors recognizing their current momentum.

Jerash has been reducing their risk as customer diversification is improving: VF Corporation was still 57% of nine-month sales, but that was down from 67% last year, while New Balance, Acushnet, Hansoll, and other customers contributed more meaningfully.

As an apparent show of confidence in their profitabl growth, Jerash has implemented a regular quarterly dividend of US$0.05 per share or around 6% annually at the current share price.

The reward case is that Jerash may be moving from a low-margin, lumpy apparel manufacturer into a more diversified, higher-utilization manufacturing platform. If they can produce $185M revenue in 2027 with ~15% EBITDA margins that should command more than their current $44M market cap.

Potential Risks: This is still a low-margin apparel manufacturer, so small margin changes can have an outsized impact on earnings. Right now I am somewhat concerned that shipping and insurance costs through the Red Sea may be impacting either margins or demand, and considering my “bull case” relies on margin expansion - this needs to be monitored closely.

Customer concentration also remains real. VF Corporation alone represented 57% of nine-month sales, and the U.S. represented 85% of revenue. Tariffs are another variable: U.S. tariffs on imports from Jordan had moved to 15%, and while customers typically pay the tariff, demand can still be affected by Jordan’s relative tariff position versus other sourcing countries.

⁉️ Question for Planet MicroCap: If Q4 revenue grows 23% to 26%, how much of that growth should convert into operating income and cash flow, and what is the realistic normalized gross margin for the business?

Paying subscribers ⏫ receive access to the Common Sense Investing discord with daily research and discussion on microcap stocks and weekly member livestreams.

Usio (NASDAQ: USIO)

Market Cap: ~$42M

Q1 FY2026 Revenue: $25.5M

Q1 FY2026 Revenue Growth: +16%

Q1 FY2026 Adjusted EBITDA: $0.8M

Cash: $7.7M

Debt: Minimal

Usio is a small payments company providing ACH, card, prepaid, output solutions, and embedded payment capabilities. In laymen’s terms it’s a payment company and here is their website for more clarification.

Payments companies can be attractive when they scale because processing volume can grow faster than fixed costs. Basically when things go well, they can go very well with exponential increases to profits and cash.

They can also be frustrating when gross margin is thin and management always promises improving margins that never consistently show up.

Q1 2026 was one of Usio’s cleaner quarters. Revenue increased 16% to $25.5M, total payment dollars processed increased 28%, transactions processed increased 22%, operating income turned positive at $0.2M, adjusted EBITDA was $0.8M, and cash increased to $7.7M even after share repurchases. When a payments processor has a quarter like USIO’s Q1 it’s at least worth putting on the watchlist and asking some questions.

Potential Rewards: The potential reward is operating leverage. If Usio can grow payment volume and revenue without bloating SG&A, the earnings profile can improve quickly from a low base. The company also repurchased shares, which is rare for a tiny payments company and suggests at least some capital allocation awareness.

Potential Risks: Gross margin fell to 20.2% from 21.9%, and prepaid card services revenue declined. Adjusted EBITDA is positive, but still modest. This is not yet a high-margin fintech compounder. It is a small, high risk, improving payments business that showed one quarter of improvement but still needs to prove durable cash generation.

⁉️ Question for Planet MicroCap:

Fool me once - shame on you.

Fool me twice - shame on me.

I have never been a shareholder of USIO before, but I know other people who have, and have been disappointed in the past with guidance that was missed. I think the question for USIO management is how are they going to convince people this time is different?

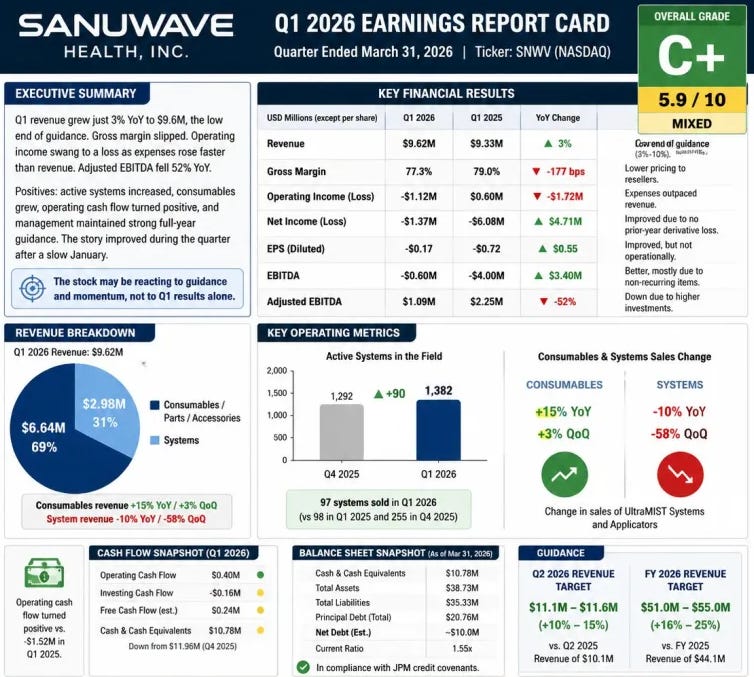

SANUWAVE Health (NASDAQ: SNWV)

Market Cap: ~$127M

Q1 FY2026 Revenue: $9.6M

Q1 FY2026 Revenue Growth: +3.1%

Q1 FY2026 Gross Margin: 77.3%

Q1 FY2026 Operating Loss: $1.1M

Cash: ~$10.8M

SANUWAVE is a medical device company focused on advanced wound care, including its UltraMIST system. This is the type of company that can get interesting if recurring consumable revenue grows, gross margins stay high, and the installed base expands.

However it’s also down a whopping 68% from 52-week highs, a massive loss for any shareholders still holding. So why the hell is Sanuwave in this article?

Sanuwave didn’t fall apart because of poor execution. The bigger issue was major changes to the wound-care market. New reimbursement pressure around skin-substitute products made providers more cautious, and that hesitation bled into the broader advanced wound-care ecosystem. Sanuwave was not the direct target, but it still sells into that same market, so customers slowed down, and deals were delayed.

The interesting thing for me, is these changes didn’t stop Sanuwave’s growth, it just slowed them down - and brought share price down to more reasonable levels. I was never a shareholder of Sanuwave because I thought $45 was crazy high, and I thought $35 was very high, and then I thought $25 was still too high.

As people changed their future growth models on Sanuwave from 35% growth down to just 15% growth, it also crashed the share price down to under $15. Now I’m wondering if Sanuwave isn’t “too cheap to ignore”.

If recurring consumables grow, gross margins stay high, and the installed base expands then Sanuwave still looks like a high quality business, just with less explosive growth than the market expected.

Potential Rewards: The core Sanuwave business hasn’t changed despite the macro-challenges. It has the kind of high gross margin profile investors like to see, and a recurring consumable revenue that can produce very high quality earnings as it scales. The company also operates in a large and important wound-care market where better outcomes can matter economically. There is still some risk here, especially since share price has been a falling knife for 11 months now (ouch!) but I have to admit as share price continues to drop Sanuwave actually looks more appealing to me, not less.

Potential Risks: The weak Q1 earnings is a problem. When share price has been dropping for 11 months straight, weak earnings and “trust me bro - the future will be better” isn’t exactly the inflection point desperate shareholders were hoping for.

The argument of “high gross margin” also falls apart when operating expenses grow faster than revenue.

Reimbursement dynamics, sales execution, reseller pricing, and clinical adoption all need watching. Unfortunately Sanuwave is now a closely monitored execution story and not a clearly improving winner.

Still good enough to make this list though.

⁉️ Question for Planet MicroCap: What is the clearest leading indicator that the macro-changes have been absorbed, and Sanuwave is going to start recovering?

Paragon Advanced Labs (TSXV: PALS)

Market Cap: ~C$79M

Q1 FY2026 Revenue: ~C$2.2M

FY2025 Revenue: C$4.37M for nine-month period

Business: Mining assay and analytical lab services

Paragon Advanced Labs is one of the more unusual names on this list. The company provides analytical technologies and lab services to the mining industry, including PhotonAssay technology. That means Paragon is not a miner. It is a picks-and-shovels style lab infrastructure business serving the mining and exploration ecosystem.

The story is early but interesting. Volatile and risky, and has recently faced two major challenges pushing its share price down.

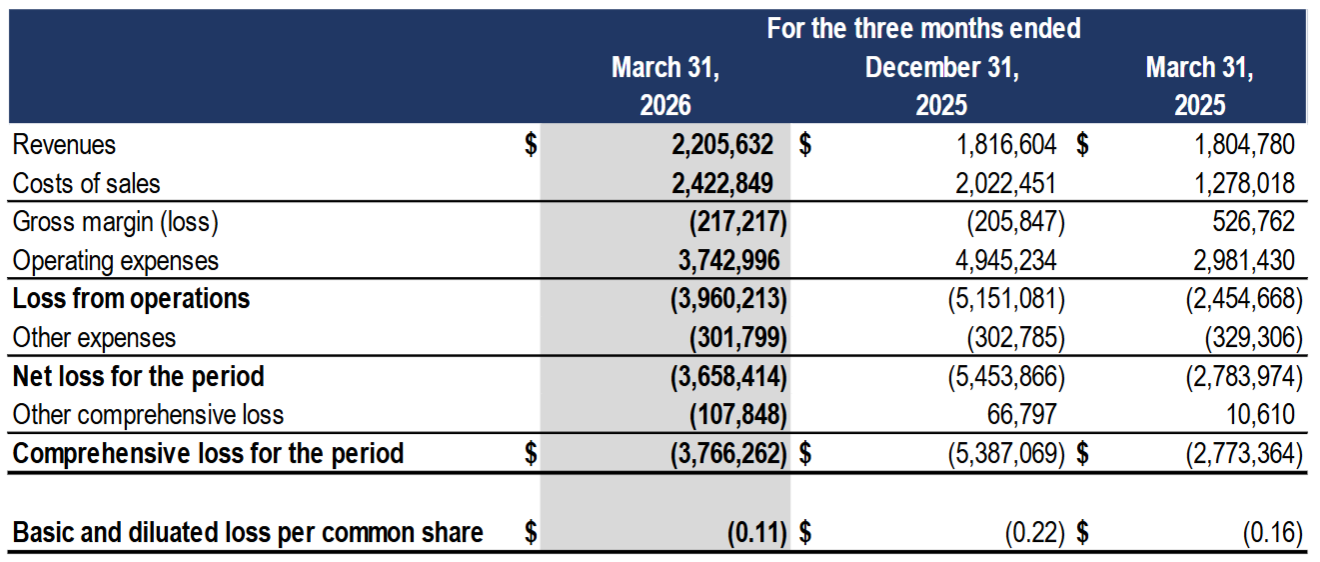

ONE - Paragon completed its RTO and began trading on the TSXV in December 2025. It has grown its PhotonAssay footprint to three machines across Hamilton, Surrey, and Sparks, and it is expanding sample prep and geochemical capacity. FY2025 revenue was C$4.37M for the nine-month period, and Q1 FY2026 revenue was expected to increase meaningfully from the prior quarter as a major client relationship ramped. That didn’t really happen. Q1 showed growth, but less than the market expected with delays being the focus of earnings and making shareholders worry they modeled the growth too aggressively.

TWO - In addition, Paragon’s CEO has also come under some critical questioning, as during his career and gaining experience for this CEO position, he was on the board of a couple companies that didn’t perform very well. One actually went bankrupt. This is the type of thing that gets classified as a “nothing burger” when your company is executing and shareholders are happy. However, when delays are causing higher than expected losses and potentially higher future dilution - that’s when all the skeleton’s in the closet get dug up and re-autopsied.

Potential Rewards: If Paragon becomes a real lab network with high utilization, recurring customer demand, and better margins as capacity fills, the upside could be meaningful. Mining assay bottlenecks are real, and faster analysis can matter for exploration teams. This is the kind of niche infrastructure story that can be overlooked early. Winning should create more winning with Paragon, as they will continue to receive capital from large investors to grow quickly.

Potential Risks: They don’t appear to be winning yet. After gaining some attention from investors as a potential long-term winning company, share price ran from C$1.60 all the way up to C$4.50 but with the delays and additional scrutiny suddenly share price has dropped to C$2.30 and worried shareholders. Paragon is still very early. Revenue is small, losses are material, and the company needs capital, utilization, and execution. Capacity expansion sounds great, but idle capacity is expensive. Investors need to see improvement soon or people will start talking about “just another failed RTO”.

For more information on Paragon I will direct you to this free article on substack from Sergio Heiber ⏫ LINK HERE

⁉️ Question for Planet MicroCap: Show me exactly what you believe has been “execution wins” for Paragon that should give me conviction to hold through downturns?

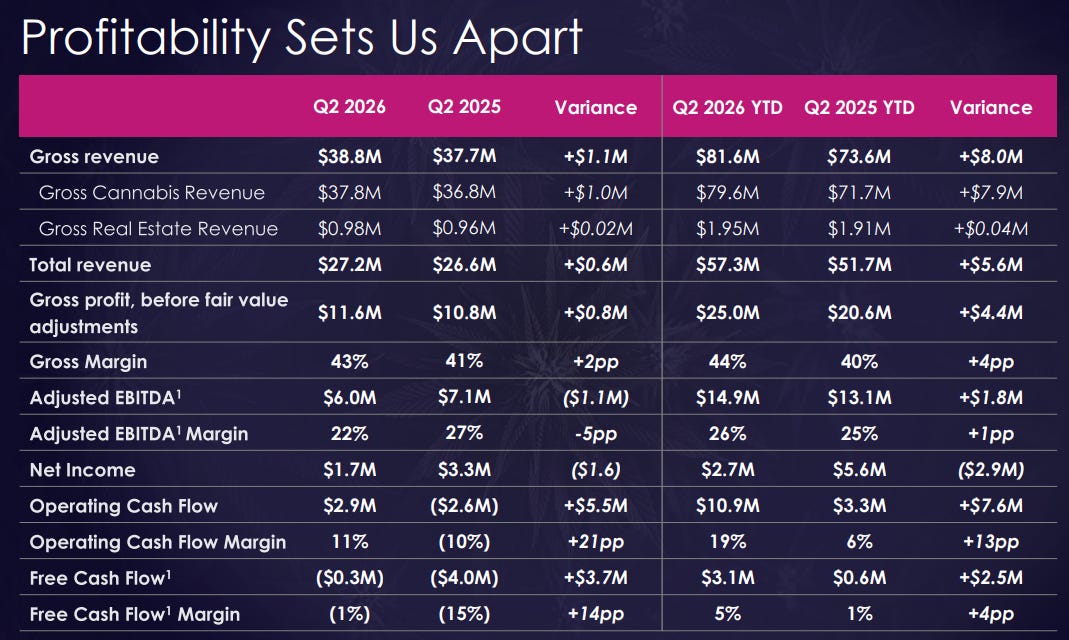

Cannara Biotech (TSX: LOVE)

Market Cap: ~C$159M

Shares Outstanding: ~98.8M

H1 FY2026 Revenue: C$57.3M

H1 FY2026 Adjusted EBITDA: C$14.9M

H1 FY2026 Operating Cash Flow: C$10.9M

H1 FY2026 Free Cash Flow: C$1.5M

Cannara has a very simple business as a Canadian licensed cannabis producer operating mostly in Quebec capturing approximately 14% of the Quebec market and expanding nationally across Canada where they have approximately 4% of the legal cannabis market.

The problem is not many people care. Cannabis has been the most hated investment sector in recent memory. The cannabis hype was huge, and when the bottom fell out investors either lost money, or watched as other people lost.

However here we are in 2026. The market doesn’t realize the best cannabis companies have clearly risen to the top, and that is because the best (most profitable) cannabis companies are all in the microcap space. If you just ignore the whole “cannabis stock” issue you will find a simple business that is capturing market share by producing and selling a profitable and recession proof product more efficiently than their larger competition.

Potential Rewards: There are basically two potential drivers of future returns for Cannara. One is company specific, and the other is industry specific.

If Cannara can keep expanding market share while maintaining gross margin and converting EBITDA into cash, the stock could not only eventually earn a better multiple than the average cannabis ticker, but also eventually (long term) earn a better multiple as the headwinds against the cannabis sector start turning.

When will cannabis headwinds switch to tailwinds? I have no idea. That’s why if you are looking at the cannabis space I think it’s smart to look for cleaner financial operators that can survive a bad market without having to dilute shareholders just to pay the bills. Cannara has been one of those cleaner operators.

So I am watching for company specific execution. They are investing heavily in capacity, and if returns on that capital are actually attractive then it will be a huge boost for Cannara and “trust” in the management team. On the macro level I keep wondering how long before the USA legalizes cannabis.

Potential Risks: This is still cannabis. Regulatory risk, pricing pressure, excise taxes, category competition, and there is still risk invested capital doesn’t produce returns. You can see the risk in share price lately. Earnings and cashflow have been a positive for Cannara, but Q2 earnings was a “miss” and share price has been trickling down. The key question is whether expansion capex like the current Valleyfield investments creates per-share value or just makes the company larger.

Here is their weaker Q2:

Q2 FY2026 Revenue: C$27.2M (Down 9.6% from Q1)

Q2 FY2026 Adjusted EBITDA: C$6.0M (Down 31.8% from Q1)

Q2 FY2026 Operating Cash Flow: C$2.9M (Down 63.8% from Q1)

Q2 FY2026 Free Cash Flow: negative C$0.3M (Down $3M)

⁉️ Question for Planet MicroCap: What return on invested capital should shareholders expect from the Valleyfield expansion, and when should that investment clearly show up in free cash flow per share?

Final Thoughts

The common thread across these five companies is simple: each has something worth watching to make this list, but none are perfect setups that deserve blind trust.

Cannara needs to prove cannabis cash flow can survive expansion. Jerash needs to navigate tariff and shipping concerns. Usio needs consistent operating leverage instead of one or two good quarters. Sanuwave needs recurring revenue to outrun expenses. Paragon needs to somehow build trust and conviction despite having no real history.

Pick your poison! Recently I was talking about investing strategies and unfortunately it’s hard to find the perfect company and stock. Believe it or not, there aren’t many A+ companies out there with a cheap share price. Investing involves compromise, and figuring out what risk you are willing to take, because the upside potential is high enough.

That is what makes Planet MicroCap useful. The goal is not to collect management stories. The goal is to ask uncomfortable questions and find out which risks may be overshadowed by quality and potential.

Below is my full list for paying members ⬇️ who get access to the discord where I am finding, researching, and discussing microcap stocks every day.

If you are currently a paying subscriber of SubStack and you have NOT joined the discord yet. Please send me an email at commonsenseinvestingman@gmail.com and I can send you a direct link to join.

commonsenseinvestingman@gmail.com

Have you looked at Thermal Energy International? They are presenting next week. Can we get your thoughts?

Thanks for your review and shout out to my article on Paragon. The company where CEO Peter was chairman of the board and quickly went bankrupt is a yellow flag as is the cleaning up the balance sheet after getting rated as a going concern. The technology seems like a no brainer from everything I’ve read but I’m going to need to hear the right answers next week.