MIND Technology (NSDQ: MIND) Update & Opportunity

Profitable Growth at a Reasonable Price

What value do you place on profitable growth?

Mind Technology is trading for approximately 6.5x EV/EBITDA after reporting 28% revenue growth in 2025 and a strong inflection to profitability with net income increasing from $274,000 (2024) to $5,100,000 (2025) 🚀

One thing I love about microcap stocks is something that most investors hate - volatility.

For a retail investor, researching and taking advantage of mispriced opportunities is one of the best and most explosive ways to make money in micrcocaps.

💵 The interesting thing with microcap stocks is “mispricing” doesn’t necessarily just happen once. Sometimes they give us multiple opportunities to buy “cheap”.

I don’t think I have to explain this in much detail right now, as we all have our favorite stock that went up 100% until January 2025 when Trump started a global trade war and now your favorite stock is down 50%. If you don’t like the price of a microcap stock, just wait a few weeks.

😡 While this is upsetting (especially for “buy and hold” investors who might see the share price drop as “losing money”) the volatility presents very good opportunity for investors willing to trim the tops, and buy the bottoms. The trick is finding the best companies that will go back up in price again, and make money.

For me, not many stocks are an example of this more than Mind Technology (NSDQ: MIND). After buying MIND for $4 in Nov-2024 it rocket up to over $10 Feb-2025 (where I trimmed) and then fell down to $6 by April-2025 because of … market fear?

Mind has already made shareholders a lot of money in 2024.

Can they do it again in 2025? Let’s take a look.

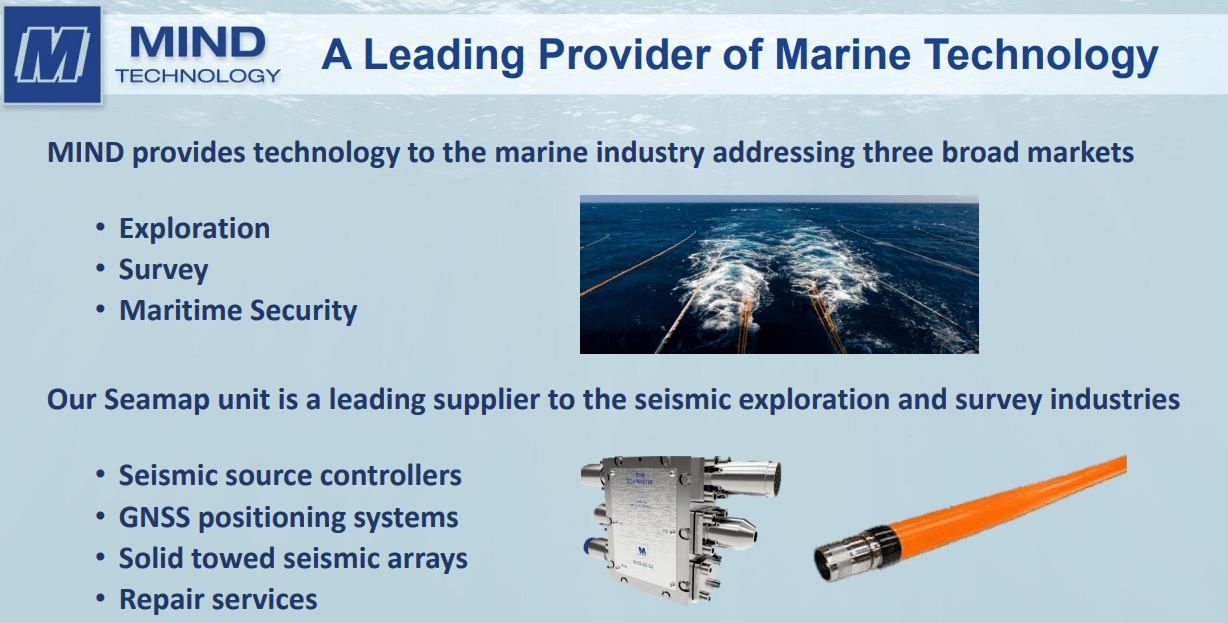

MIND Technology: What They Do

A niche but potentially lucrative segment, providing technology and solutions for exploration, survey, and defense applications within the oceanographic, hydrographic, seismic, and maritime security industries. Their Seamap product line, which includes GunLink seismic source controllers, BuoyLink positioning systems, and SeaLink streamer systems, has become an essential part of operations for seismic exploration contractors and marine survey companies globally.

Efficient Production and Cost Control

One of MIND Technology’s strengths lies in its operational efficiency and thoughtful approach to production. In recent quarters, the company has implemented price increases of 5-10% across most product lines, strategically offsetting rising material costs and supply chain challenges. Additionally, improved production efficiencies have helped maintain a robust gross margin of 45%, up from 44% the previous year.

With most of their manufacturing based in Malaysia and Singapore, MIND has been largely insulated from tariff issues (contrary to what some investors may have perceived when selling shares). This strategic geographical setup not only reduces risk but also allows the company to focus on maintaining profitability even in a volatile economic environment.

Even if the end-game for Trump is 10% tariffs on everything entering the United States and there is no way to avoid that - MIND’s primary revenue sources geographically are Europe and Asia-Pacific, with manufacturing and repairs done in the USA (which is a service, and shouldn’t be tariff exposed). The CEO has stated that tariffs would have little to no impact on MIND.

While their technology might not be classified as "cutting edge," it is reliable, field-proven, and highly regarded within the industry. You could make the argument their GunLink product has an international “moat”, while the company humbly states they have a “dominant market position”. This stability gives MIND a solid foundation to build upon as they explore new applications, particularly in the defense sector and the burgeoning subsea cable industry.

A Disciplined Approach to Capital Management

It’s refreshing to see a management team that understands capital allocation. Not only is cash treated as an asset, but so are shares and the overall quality of the business.

In fiscal 2025, MIND reported a net income of $5.1 million, a marked improvement from just $274,000 in fiscal 2024. This leap reflects both disciplined financial management and increased demand for their products. The company’s debt-free balance sheet, with $5.3 million in cash, further underscores their focus on maintaining financial health without over-leveraging. They’ve also kept administrative costs in check, reducing these expenses by 7% primarily through headcount optimization.

Mind Technology (NSDQ: MIND) reported full year 2025 earnings April 22, 2025

Significant improvement in 2025 that isn’t reflected in share price.

While Covid was an obvious disaster (and left off this chart) MIND’s growth since Covid has been substantial. With 87.6% growth in revenue over 2-years, and even more impressive a 312.9% growth in backlog during that time.

While the market hit “extreme fear” in 2025 thanks to Trump tariffs, panicking investors highlighted the declining backlog in fiscal 2026 as a concern for MIND. However, the backlog is already up to $32.8M for 2026 and a single large contract can easily return it to high growth.

But what is revenue growth and backlog without a transition to the bottom line! In 2025 MIND not only was able to grow the company significantly, they managed it while improving margins, something most microcap investors love to see. Suggesting that company promises towards “operational efficiency” are turning into tangible results.

Q1 = $1.514M adjusted EBITDA on $9.678M revenue = 15.6%

Q4 = $3.017M adjusted EBITDA on $15.044M revenue = 20.0%

At the surface MIND Technology is a well managed, profitable and growing microcap in the ocean exploration niche. Basically a perfect company (for a microcap) 😉

So why the extreme volatility in share price?

Timeline of Volatility

1️⃣ Conversion of Preferred Shareholders to Common Shareholders

For most of 2024 Mind Technology was uninvestible. Despite some growth in sales, the company share structure was choked to death limited by large numbers of preferred shares collecting dividends. Where basically every dollar of profit was being given away - and not available for company growth.

The company in what can only be described as a small miracle with incredible negotiation skills - managed to convince preferred shareholders to exchange each preferred share for 3.9 common shares. Brilliant! The company now had 8 million common shares and a clean share structure with no drag -a fresh start. Share price rocketed up from $3.50 to $6.00 USD.

2️⃣ Valuation Expansion Up to “Fair Value”

After the jump from $3 to $6 share price continued upwards to almost $11 - and I think that was well deserved. After the preferred share conversion, MIND is a profitable and growing company with cash and no debt (on the Nasdaq) - that’s worth a fair valuation. At $10 back in February MIND was still trading for under 2x sales and 15x earnings. It wasn’t cheap anymore, but not expensive either.

Unfortunately for MIND shareholders holding long, price dropped for (probably) the following reasons:

General market crash: Which caused a sell off in high risk microcaps. With MIND’s short history since the preferred share conversion, it was “high risk”.

Tariffs: Implemented (briefly) on Singapore and Malaysia where MIND manufactures their products. Despite this having almost no effect on MIND, it didn’t help already worried shareholders.

Trimming: All shareholders made sizable profits moving from $3 to $10 and there was

some trimminglots of trimming. I think even in a good market, price would have fallen due to natural trimming of position sizes. However, once the market turned for the worse and MIND shares started dropping on volume - there was plenty of selling from the preferred shareholders, and then even institutions.

Investing Strategy: When you combine a “risk off” market, with a stock in your portfolio that’s up 200% (but is now dropping) it’s an absolute “no-brainer” to trim or sell the stock. It was just an overall poor setup for Mind Technology back in February of 2025.

Mind Technology Today - Strong Financials in 2025

Since the drop from $10 to $5 there has been one notable event that helped recover share price, and get me optimistic again in 2025 - EARNINGS. Financials matter!

MIND Technology April 22nd 2025 reported significantly improved financial results in fiscal 2025 compared to the previous year:

Net income of $5.1 million, a substantial improvement from a net income of just $274,000 in fiscal 2024.

Operating income also surged from $518,000 in 2024 to $6.8 million in 2025, driven primarily by increased revenue from the Seamap product lines and strategic cost-saving measures.

Revenue for 2025 reached $46.9 million, up from $36.5 million in 2024, marking a year-over-year growth of 28%. This increase was primarily attributed to higher demand for the company’s Seamap Marine Products, including GunLink seismic source controllers, BuoyLink positioning systems, and SeaLink streamer systems.

Strong gross profit margin of 45%, compared to 44% in the prior year, benefiting from production efficiencies despite rising warranty costs.

Significant rise in Adjusted EBITDA, reaching $8.2 million in 2025, compared to $2.3 million in 2024, representing a remarkable 256% increase.

Debt-free, maintaining $5.3 million in cash, reflecting improved operational cash flow of $651,000 compared to a cash outflow of $4.97 million in the prior year.

Despite challenges such as increased costs due to inflation and supply chain issues, the company’s strategic pricing adjustments (5-10% increase on most products) and cost control measures helped maintain profitability. MIND Technology also streamlined its operations by reducing administrative expenses by 7%, primarily through headcount reductions.

With a strong backlog of approximately $16 million and an additional $15.9 million in new orders received post-year-end, MIND Technology enters fiscal 2026 with positive momentum. Management remains optimistic about maintaining profitability, focusing on expanding its market presence through product innovation and operational efficiency.

Positioned for Growth in Fiscal 2026

MIND Technology (NASDAQ: MIND) is entering fiscal 2026 with a renewed sense of momentum. After reporting a record-breaking fiscal year in 2025, the company has set itself up for continued growth.

The recent earnings call highlighted a $16 million backlog, supported by an additional $15.9 million in new orders post-year-end. With robust demand for their Seamap product lines, including GunLink source controllers, BuoyLink positioning systems, and SeaLink streamer systems, MIND's strategic focus on operational efficiency and product innovation is already paying off with sustained growth.

One of MIND's most promising aspects is its strong aftermarket revenue (regular servicing of their customers products), comprising approximately 40% of the company’s total income. This recurring revenue stream showcases the company’s ability to capitalize on its expanding installed base, where increased product sales the past year should transition to increased aftermarket sales in future years.

CFO Mark Cox's emphasis on maintaining a 45% gross profit margin through price increases and production efficiencies adds to the positive outlook. Additionally, MIND’s debt-free balance sheet and a cash position of $5.3 million offer financial stability as the company navigates potential market fluctuations.

While MIND Technology has faced market volatility, including a significant share price drop since February, the company’s fundamental improvements and clear growth path signal potential upside. The current valuation, with a current EV/EBITDA ratio of around 6.5x and a forward EV/EBITDA ratio of 5.1x suggests that the market may be undervaluing the stock, especially given its four consecutive profitable quarters and improved capital structure.

For investors looking at microcap marine technology stocks, MIND's combination of strong financial performance and strategic growth initiatives make it a compelling watch for the coming year.

Additional Information and Notes on MIND Technology

In addition to the attractive profitable growth MIND offers, it’s interesting to note that the company has engaged Lucid Capital Markets to explore ways to grow the business, or potentially sell the business. With the CEO stating the following in the full year 2025 press release:

I am very pleased with where MIND is positioned today. We have stabilized the company, restored it to profitability and positioned ourselves to take advantage of opportunities within our existing and future markets," added Capps. "However, we are still a small company, which presents certain challenges. We believe that to maximize stockholder value, MIND needs additional scale. We have identified organic growth opportunities that could help grow the Company. However, we also believe there are several other ways to achieve additional scale, including acquiring assets or businesses, combining with other organizations, or even an outright sale of the Company. All of these options are open to us, and we intend to investigate and analyze them. To assist us with this effort, we have retained Lucid Capital Markets LLC. - Rob Capps, MIND's President and Chief Executive Officer

So while retail investors are selling, institutional investors are buying.

Finally, I have to say that MIND is getting this article from me today due to the current setup. After the recent dip, share price has partially recovered and has been consolidating for some time. With Q1 earnings expected in the second week of June (approximately one month from the writing of this article) I wonder if share price isn’t getting ready to bench up.

Ultimately I like a company that gives me multiple ways to make money. They might continue along like normal, growing the company and increasing it’s value slowly over time. They might look to an acquisition to grow a little quicker now that they have cash and working capital. Or they might decide to sell at a nice premium. Due to the improved share structure and strong balance sheet, I see the risk as being fairly low with MIND, while the potential is looking good.

⏸️ If you’re a new microcap investor hoping to learn, or an experience microcap investor looking to talk stocks on a moderated platform with other microcap investors, consider joining my patreon.

👍The patreon gives you access to a “patreon discord” with daily updates and live chat about microcap stocks, patreon only livestreams, and lots more of “Common Sense Investing”. The “Friends of the Channel” option gets everything first, including these articles, and any other content I expand to in the future. Thanks for reading! LINK to Patreon HERE

Seriously, this is NOT financial advice.

I mean it. None of this is financial advice—I say it all the time, and I genuinely mean it. I don’t know you. I don’t know your experience level, risk tolerance, debt situation, or anything else about your financial position. So please, don’t buy, sell, or hold a stock just because of my opinion in this article.

I’ve been wrong plenty of times, and I strongly encourage everyone to invest within their own capabilities and consult a financial advisor if needed.

Thank you! 🙏