Planet Microcap Showcase Preview (I-K)

Introducing Stocks A to Z

I will be writing several articles introducing (briefly) all 100 stocks attending the Planet Microcap Showcase this April 22-24 in Vegas, to give you a taste of what companies are showing up and which ones may interest you the most. The final article will be my personal “Top 10” describing the stocks I think the 500 microcap investors attending the event will have the most interest in.

Article #1 covering all stocks in the A’s (LINK HERE)

Article #2 covering stocks B to C (LINK HERE)

Article #3 covering stocks D to F (LINK HERE)

Article #3 covering stocks G to I (LINK HERE)

This is not financial advice. I like to sprinkle some of my own personality and opinion into discussion of stocks, and nobody should interpret that as any kind of solicitation to buy or sell a stock. This is simply an article to help you with research, and start discussion.

Enough small talk… there are a lot of stocks to introduce.

illumin Holdings Inc. (TSX: ILLM) illumin.com/

What they do: Services (advertising) a technology company, provides digital media solutions in the United States, Canada, Europe, Latin America, and internationally. The company offers a programmatic marketing platform that enables advertisers to connect with their audiences.

Potential rewards: How much do you know about AdTech stocks? Illumin is a story I have been following for a long time. Illumin diluted shareholders back in 2021 when share price was high (brilliant move) giving them $100M in cash. Since 2021 they have been burning that cash transitioning away from their legacy person-to-person advertising platform (AcuityAds - their former name) and into their new AI driven programmatic advertising platform (Illumin - their new name). That transition was finally paying off when they reported 2024 earning (three weeks ago) with 35% Q4 growth and 11% full year growth, as well as no more cash burn, and share price rocketed up from $2 to $3 on the news. Unfortunately while AdTech stocks had a great 2024 and investors made money, the Trump tariffs have driven fear into the market and the narrative I keep hearing is “recession is coming and AdTech stocks will suffer” causing ILLM shares to crash below $2 completely ignoring their 2024 improvements. If you don’t believe this narrative, then Illumin now has a great balance sheet and some recent strong growth.

Potential risks: For me personally I see two risks. 1) That the narrative is true and that AdTech spending will get reduced in 2025 and AdTech stocks will see negative growth. Considering that Illumin just transitioned to having a good year, this would be significantly hard on them. And 2) Illumin lost a lot of trust with investors. April 2024 Illumin’s long time CEO stepped down to bring in a complete outsider to try and change this narrative, but you can still find the distrust on social media where despite Illumin showing a greatly improved 2024 many investors are stilling digging hard into earnings and focusing on the remaining challenges, rather than the recent improvements. It’s caused lots of people to be trading this stock, and few people buying to hold.

Innovative Food Holdings (OTCQB: IVFH) www.ivfh.com

What they do: Consumer (food service distribution) distributes specialty food and food related products to restaurants, hotels, country clubs, national chain accounts, casinos, hospitals, and catering houses in the United States.

Potential rewards: Shareholders of IVFH (that I have spoken to) LOVE this company and stock, and probably for good reason as for an OTCQB stock IVFH has been consistently improving and share price kept benching up from <$1 to >$3 for 150% gains (until this recent tariff sell-off of course). Why? In 2024 IVFH underwent a significant transformation as they sold their direct-to-consumer e-commerce platform signaling a deliberate shift away from the consumer market to a more business-to-business model. These maneuvers were part of a broader strategy to streamline operations and position the company for future growth, and so far it looks to be working as their full year 2024 earnings showed 2.5% revenue growth (11% of that organic) and an inflection point from GAAP net losses in 2023 to a positive GAAP net income of $2.5M. The improvement is noticeable, and shareholders have a lot of confidence in IVFH’s management team to continue this trend of improvement and growth.

Potential risks: Not the companies fault, but valuation of IVFH is a bit “frothy” especially for an OTCQB stock and definitely in a bear market. $100M market cap for $2.5M net income on $74M of revenue isn’t “cheap” and while I like the company I wonder how many investors will be buying IVFH right now when there are a other equally good companies at objectively cheaper prices. IVFH management at MCC Vegas has a great opportunity to convince investors the valuation is fair based on future growth and continued execution.

Intellicheck (NSDQGM: IDN) www.intellicheck.com

What they do: Technology (identity validation) a technology company, provides on-demand digital identity validation solutions for KYC, fraud, and age verification needs in North America.

Potential rewards: Disclaimer, this is another company/stock I have never heard of before, so consider my opinion that of a “first timer”. I am struggling to find the potential rewards of IDN, and I think share price being down 30% in 12-months confirms other investors are having the same problem I am. What’s the upside? In 2024 IDN grew revenues by $1M or about 6% to a total of $19.9M. In the meantime they reduced their expenses by ~$500,000 resulting in an improvement of $1.5M compared to 2023, but the company still wasn’t profitable posting a $0.05 loss per share in 2024 (compared to a $0.10 loss per share in 2023). Very slow moving company making very minor improvements every year, maybe it’s a sleeper opportunity.

Potential risks: While I don’t want to undermine the improvements made by IDN in 2024 (the company grew revenue and reduced expenses, and that’s always a win) unfortunately those aren’t the types of numbers that attract many microcap investors. Most of us are investing in microcaps to outperform mega-cap stocks, and we’re looking for growth either top line or bottom line of 15% or much more. At best “6% growth and still unprofitable” is more of a “bottom of the watchlist” type of stock.

Interlink Electronics, Inc. (NSDQCM: LINK) www.interlinkelectronics.com/

What they do: Technology (electronic components) designs, develops, manufactures, and sells force-sensing and gas-sensing technologies that incorporate proprietary materials technology, firmware, and software into sensor-based products and custom sensor system solutions.

Potential rewards: Interlink is going to need to tell investors what the potential reward is. They reported their full year 2024 earnings where revenue fell over 15% and their net losses grew over 600% to $2M. The CEO said “2024 marked the beginning of an exciting new chapter for Interlink” and I think this needs to be explained.

Potential risks: Despite what looks to be a disappointing 2024 for Interlink, valuation is still priced for significant improvement as this is a $57M market cap stock that just reported decreasing $11.6M of revenue and $2M of net losses. Shareholders must have pretty high expectations of Interlinks future, and if they don’t deliver… ?

Intermap Technologies Corporation (TSX: IMP) www.intermap.com/investors

What they do: Technology (software application) a geospatial intelligence company, provides various geospatial solutions and analytics in the United States, Canada, the Asia Pacific, and Europe.

Potential rewards: Finally Intermap to the rescue with a stock I’m a bit more bullish on. A huge winner in 2024 going from $0.50 CAD to a high of $2.83 (and yes, I thought share price was getting a bit too high). Thankfully Donald Trump to the rescue! With global tariffs crashing the market and potentially getting shares of IMP back into some buying ranges for many microcap investors. Intermap just reported 2024 earnings of $17.6M on $2.46M of net income or around $0.054 EPS which is pretty good and exciting. But what’s better is their 2025 guidance of $30-35M revenue with 28% EBITDA margins. There aren’t many stocks in 2025 (with all the discussion about global recessions) that are guiding for potentially 100% growth in 2025, on top of their already profitable business model. Attractive looking company.

Potential risks: The only speedbump in the Intermap story might still be Donald Trump and global recession. Intermap did give their 2025 guidance March 27th, so only days before Trump announced global tariffs, and I expect Intermap has factored tariffs into their guidance…. but right now with the markets crashing, I’m pretty sure microcap investors at MCC Vegas would like management to “double down” on guidance and confirm that nothing has changed in the current environment, because with a $90M market cap and only $30-35M in revenue for 2025 anyone buying shares of Intermap are still paying for growth that hasn’t occurred yet.

Intouch Insight Ltd. (TSXV: INX) intouchinsight.com

What they do: Services (customer experience management) a complete portfolio of customer experience management (CEM) products and services that help global brands delight their customers, strengthen brand reputation and improve financial performance.

Potential rewards: Always a bridesmaid, never a bride: I have looked at INX at least a dozen times over the past few years and never bought shares. Maybe now is different, because the real potential in INX is they are a $10M market cap nanocap stock that doesn’t need much improvement (or attention) to get their market cap rocking higher. And I have to say, their 2024 full year earnings have me circling back to INX as they reported 11% revenue growth (7% SaaS growth) on top of a 46% EBITDA gain, and a net income of $1.4M compared to a loss of $384,000 last year. It’s a record year for INX, could potentially be indicating more consistent growth with product-market fit, and is worth discussing further with management. Company is improving, share price has done nothing, and I like that setup as INX appears to be a fairly “cheap” low risk stock especially at Donald Trump prices.

Potential risks: Talk about bad timing for INX, and I mean BAD timing. Share price was up to $0.68 CAD before the bottom fell out of the market dragging it down to $0.50 .. and then this little nanocap stock that nobody cares about released pretty good 2024 earnings with significant improvements on Trumps “Liberation Day” the worst stock market crash since Covid was announced. Share price is back down to $0.40 and despite this company looking better, I wonder if they ever get the attention they deserve? And of course whether they can continue their current growth trajectory, that too!

Ispire Technology Inc. (NSDQCM: ISPR) ispiretechnology.com/

What they do: Consumer (tobacco) researches, develops, designs, commercializes, sales, markets, and distributes e-cigarettes and cannabis vaping products worldwide.

Potential rewards: Another stock I’m researching for the first time, so take that with a grain of salt, but it’s tough being a cannabis stock these days. Ispire’s market cap has fallen from $658M in 2023 to a $176M market cap on top of $164M revenue (if you annualize their Q2 earnings). That may be the potential reward here, as I know many cannabis investors looking to time the bottom on cannabis stocks, saying that the market in general is really bad right now - and when things are this bad the only news can be good news. The company is expanding internationally and I see they already have 500 locations in South Africa and Nigeria, and I hope their market growth pays off for them some day.

Potential risks: Challenging markets usually result in challenging earnings, and Ispires’ recent Q2 earnings gave shareholders a net loss of $8M which is double the net loss of $4M from Q2-2023. Ugly. Now luckily enough it does look like Ispire has some cash (and little to no debt) which is a good thing because a financing into a tough market would be bad. However, it’s already bad for Ispire as share price is down 46% in 12-months and unless they can show improved financial performance then it’s hard to say where the bottom is.

Jewett-Cameron Trading Co. (NSDQCM: JCTC) jewettcameron.com/

What they do: Materials (lumber and wood production) engages in the manufacturing and distribution of pet, fencing, and other products. The company operates through Pet, Fencing and Other; and Industrial Wood Products segments.

Potential rewards: I’m sorry I have been trying to avoid using pictures in these articles because it makes them too long, but I couldn’t avoid attaching a picture for Jewett-Cameron as they are listed as a “lumber company” when they more accurately make pet accessories (that includes some lumber such as fencing). My first impression of JCTC is that they should get bought out by a private company. Share price is down 33% on the year as money is tight right now for people and there is less discretionary spending in pet accessories. There are cracks in the earnings as Q1-2025 reported a $700,000 net loss compared to a net income of $1.3M last year. This appears to be a good little company struggling in challenging economic (and market) conditions, and I wonder how long their little $12.5M market cap sits available before someone is willing to buy that $46.5M TTM revenue in a private equity deal.

Potential risks: Recession and less spending on discretionary pet items is obviously this company/ stocks greatest risk. Despite an already tiny $12.5M market cap, if the current trends continue to get worse for JCTC then so can their share price. This might be the greatest risk (and potential reward) for JCTC shareholders as this is too good of a company to go bankrupt, and I wonder sometimes if private equity doesn’t put on a disguise (poorer clothes and a cheaper car) and attend MCC Vegas looking for takeout candidates.

Kingsway Financial Services Inc. (NYSE: KFS) kingsway-financial.com/

What they do: Consumer (auto and truck dealerships) engages in the extended warranty and business services in the United States. It operates through two segments: Extended Warranty and Kingsway Search Xcelerator.

Potential rewards: From 2021 to 2022 Kingway grew revenue significantly from $81M to $114M and had a major inflection point going from a net loss, into a positive EPS of $1.04 and that’s impressive. However since 2022 Kingway has struggled, reporting full year 2024 earnings just a few weeks ago with $109M in revenue on a $8.3M net loss. Ouch! Considering share price is UP 295% over the past five years, and share price is only down 7% in 12-months despite weak earnings… and I have to think I’m missing something important happening with Kingway. Which means their potential reward might be more qualitative than quantitative, as I see they made a recent acquisition, and made some changes/ additions to management. The company may have to convince me what the potential is right now for Kingway.

Potential risks: There’s an article from Zack’s that best sums up my thoughts, it’s titled “Kingsway Stock Rises Despite Q4 Earnings Decline (EBITDA Improves)” which describes some of my confusion as well. Given their current $211M market cap, $109M of declining revenue, and net losses; I would have some valuation concerns should shareholder sentiment turn negative.

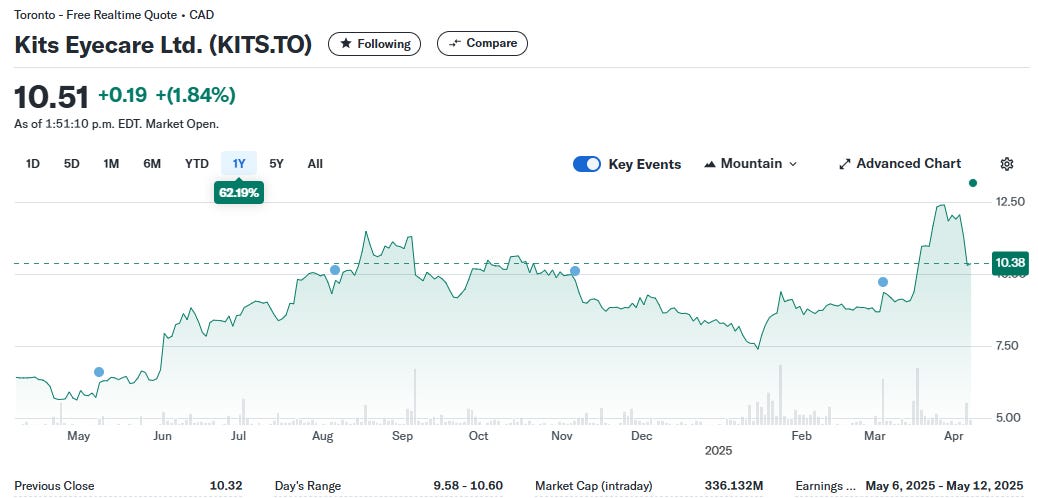

KITS Eyecare Ltd. (TSX: KITS) ir.kits.com/overview/default.aspx

What they do: Consumer (specialty retail) operates a digital eyecare platform in the United States and Canada. It manufactures progressive and contact lenses, eyeglasses, and frames under the KITS brand, as well as distributes eyewear products of various brands.

Potential rewards: Winners keep winning! KITS is one of those companies I missed out on. I sat on the sidelines as share price went from $2 in 2022 to over $10 in 2024 and congratulations to shareholders! Since then KITS has been volatile dropping 35% before rebounding up to record highs of $12.50 just days ago on March 27th. The reason share price has recovered is the same reason I didn’t buy KITS shares, their margins are so low. KITS has always been an attractive looking company with nice consistent revenue growth (32% growth in 2024), but they have always struggled converting that to anything meaningful on the bottom line with razor thin 4% adjusted EBITDA margins. Recently KITS updated their Q1-2025 guidance saying their margins are improving from 4-6% to a more reasonable 6-8% and that gives shareholders significant hope that KITS is starting to realize operating leverage and margins will continue to increase in the future. If KITS continues growing top line at this very high rate, AND can improve their margins… well that’s when winners keep winning.

Potential risks: I’m still not a shareholder of KITS so my personal opinion might be the best description of the “potential risks” (though there is a good chance I’m wrong, because I have been wrong since 2022 about KITS). I’m just not a huge fan of a low margin business in a highly competitive market. KITS sells online glasses, and if you Google “cheap glasses” you will find a dozen locations in your neighborhood (including large retail like Walmart and Costco) as well as other online companies. Lots of competition. Quantitatively, shareholders of KITS are focused on adjusted EBITDA numbers and that’s not something I’m very excited about (more of an EPS kind of guy), especially considering they only produced $6.4M of adjusted EBITDA on $159M of revenue in 2024. Great company! I’m cheering for them as I love when microcap investors make money, but I’m still on the outside looking in.

kneat.com (TSX: KSI) kneat.com/

What they do: Technology (software) designs, develops, and supplies software for data and document management within regulated environments in North America, Europe, and the Asia Pacific.

Potential rewards: Kneat had a very successful 2024 that caught the attention of a lot of good microcap investors. Consistent top line growth from $15M (2021) to $48M (TTM) but even more importantly in 2024 Kneat’s expenses were growing slower than revenue and they started to show signs of consistent strong profitability. 2024 EBITDA was $5.6M compared to an adjusted EBITDA loss of $5.7M in 2023, and when you ask if this growth is continuing Kneat’s Q4 growth was 40% revenue, 60% recurring revenue, and 48% gross profit. Stunning! Adding five large customers in 2024 I think the real potential reward for Kneat shareholders is simply how long this continued rapid growth in both top and bottom line can continue?

Potential risks: The potential risk is that growth needs to continue strong, because Kneat’s shares are priced for growth. This is a $537M market cap company with 2024 revenue of $48.9M and $5.6M EBITDA. Without doing any math myself and just looking at YahooFinance I’m seeing a price-to-sales of >10x and EV/EBITDA of >80x and I’m not sure that I’ve personally ever bought shares of a company with that high a valuation, in fact my “hard line” cutoff for price-to-sales valuation is 10, I refuse to buy any stock with a double digit P/S so unfortunately for me Kneat isn’t on my buying list, but that’s just me personally and every investor is different.

Koil Energy (OTCQB: KLNG) www.koilenergy.com/

What they do: Energy (oilfield services) an energy services company, provides equipment and support services to the energy and offshore industries. The company offers engineering and project management services, including the design, installation, and retrieval of subsea equipment and systems.

Potential rewards: Let’s start with share price being up 222% in 12-months (congratulations). While I am no expert in Koil, it’s my understanding this was a correction to their valuation based on an inflection point to profitability, and if that can continue it would be great for shareholders. For example, Koil hasn’t reported their full year 2024 earnings yet, but their Q3 reported $5.2M revenue (up 27%) and a net income of $523,000 compared to a net loss in 2023. Improvement! Given Koil is still at a reasonable $20M market cap, and I’m bullish in the industry sector they are in (offshore energy services, but not an oil company) and Koil is definitely moving up my watchlist and look forward to a presentation from management to tell their story.

Potential risks: There’s lots to discuss here. As a short-term risk Koil announced a delay to their Q4 and full year 2024 earnings, and given how bad the macro-market is right now, it’s not surprising to see share price drop 13% as I write this article. I think longer-term (and what I really want to hear from management) is the future of offshore energy. Two months ago Trump announced the opening of 625 million acres of ocean available for energy exploration (super bullish news) but since that announcement oil prices have crashed to the point I’m not sure offshore energy is even financially viable and the industry will struggle (also offshore wind-energy may be dead). I’m no expert here, I’m just giving concerns off the top of my head, but I think my concerns are valid questions that other investors will have, and need further research and discussion.

⏸️ If you’re a new microcap investor hoping to learn, or an experience microcap investor looking to talk stocks on a moderated platform with other microcap investors, consider joining my patreon.

👍The patreon gives you access to a “patreon discord” with daily updates and live chat about microcap stocks, patreon only livestreams, and lots more of “Common Sense Investing”. The “Friends of the Channel” option gets everything first, including these articles, and any other content I expand to in the future. Thanks for reading! LINK to Patreon HERE

Seriously, this is NOT financial advice.

I mean it. None of this is financial advice—I say it all the time, and I genuinely mean it. I don’t know you. I don’t know your experience level, risk tolerance, debt situation, or anything else about your financial position. So please, don’t buy, sell, or hold a stock just because of my opinion in this article.

I’ve been wrong plenty of times, and I strongly encourage everyone to invest within their own capabilities and consult a financial advisor if needed.

Thank you! 🙏