The Death of Substack

And an Introduction to Propel Holdings Stock (TSX: PRL)

I haven’t been writing much on Substack - why? Because AI is replacing me.

I see investors on social media mocking AI and saying it’s garbage. That AI simply can’t replicate an experienced human investor and real human analysis.

I disagree.

I am now fully convinced that most investors simply don’t know how to use AI, how to write effective prompts, how to train an AI to fact check it’s own inaccuracies, and are probably mostly just resistant to change.

Humans have bias. Confirmation bias. Recency bias. Overconfidence bias. Anchoring bias. Herd bias. A human author may unintentionally due to bias focus only on the positives, and ignore all the negatives.

All these issues are gone with AI.

Will AI occasionally make errors? Sure. So do humans. That’s why you have to obviously read and fact check what AI produces to ensure the best quality product, the same as you should when reading human produced content. But can AI provide 100% more research in 10% of the time? Yes. Why would you not take advantage of that?

The main complaint I have received from people using my AI prompts?

It does a poor job of being overly bullish.

I wrote my AI prompts to be skeptical and factual. The most common ‘complaint’ is “the AI didn’t factor in enough forward growth”. The AI prompts I have built do not consider the complete 100% execution of {insert speculative product or service here} … like a human does when we get overly excited about a stock and start ignoring more conservative estimates.

Is this a weakness or a strength? I consider being overly conservative a strength.

Anyway. I’ll just shut up and let you read for yourself. Here is an AI generated buy-side report for Propel Holdings (TSX: PRL) including a “Mock Investing Strategy” on point #23. I have been producing ~5-10 of these reports per week on my discord which can be accessed by paid subscribers of this Substack.

And of course none of this is financial advice, or a solicitation to buy, sell or hold Propel Holding stock. There is a full disclaimer at the bottom of the article.

Propel Holdings on the TSX ticker PRL.

$696M Market Cap with 39.36M shares outstanding and 26.71% insider ownership.

Propel pays a quarterly $0.225 dividend a 5% annual return at todays share price.

1. Investment Memo Snapshot

● Propel finished 2025 with record revenue, record ending balances, and record full-year adjusted EBITDA, but Q4 profitability deteriorated sharply because the company accelerated originations late in the quarter and absorbed the related provisioning and acquisition costs up front.

● The core bull case is that this was a timing and accounting compression quarter, not a broken model: management kept underwriting tight in Q3/Q4, saw credit trends improve late in Q4, then leaned back into growth heading into 2026.

● The key near-term reason the story still matters is funding and product expansion: Propel launched FreshLine, added a US$60 million Mesirow forward-flow commitment, then announced an additional commitment of up to US$150 million tied to FreshLine’s rollout.

● The goeasy situation is an important read-through. In March 2026, goeasy disclosed a major LendCare-related charge-off/write-down situation, historical reporting corrections, covenant waivers, higher funding spreads, and a reduced warehouse line. That likely improves the relative perception of Propel’s underwriting discipline and funding model, though it also reminds investors that this sector can re-rate violently when credit quality slips.

● My bottom line: the operating story remains attractive, but earnings quality is mixed rather than pristine because adjusted profitability still overstates underlying cash generation in a growth-lending model that consumed operating cash in 2025.

2. AI Analyst Summary

Propel is still one of the more interesting North American listed subprime/underserved-consumer fintech lenders: it has grown revenue from US$129.6 million in 2021 to US$589.8 million in 2025, increased full-year net income from US$6.6 million to US$59.5 million, and expanded into Canada, the UK, bank-partner programs, and LaaS.

But the latest quarter was not clean. Q4 2025 revenue rose 21% to US$155.8 million, while net income fell 49% to US$5.9 million and adjusted EBITDA fell 32% to US$21.6 million. Management’s explanation is plausible: tighter underwriting held back growth through much of 2025, then improved credit performance late in Q4 allowed it to accelerate originations in December, bringing forward provisioning and acquisition costs while the revenue remains to be earned over future periods. That explanation is supported by the reported figures, but it does not eliminate risk; it simply means investors need proof in Q1/Q2 2026 that margins and credit normalize as promised.

The strategic setup improved after year-end. FreshLine and the Column relationship broaden Propel’s U.S. addressable market, while Mesirow and the additional US$150 million commitment show third-party capital is still willing to fund new Propel-originated programs. That matters because this is a lender/platform that can grow only as long as it has durable capital support.

Verdict: still investable, but no longer a “just trust the compounder” story. It is now a show-me-the-margin-recovery story.

3. Company Snapshot

Propel Holdings is a Canadian-listed fintech focused on underserved consumer credit, operating through MoneyKey, CreditFresh, Fora Credit, QuidMarket, Propel Bank, and LaaS/bank-partner programs. The shares traded at C$17.86 on March 26, 2026, with a market cap of about C$702.9 million per TMX. The company had 39.36 million common shares outstanding at December 31, 2025, and 42.23 million diluted weighted-average shares for 2025. Directors and executive officers as a group beneficially owned 35.91% of outstanding shares per the 2024 AIF.

On the fundamentals side, 2025 revenue was US$589.8 million versus US$449.7 million in 2024; Q4 2025 revenue was US$155.8 million, up 21% year over year. Full-year net income was US$59.5 million and diluted EPS was US$1.41 / C$1.97; adjusted EBITDA was US$130.3 million. Year-end cash was US$23.9 million, restricted cash US$50.0 million, credit facilities US$329.6 million, and lease liabilities US$9.4 million. Loans and advances receivable ended 2025 at US$459.8 million, while ending combined loan and advance balances were US$589.5 million. Backlog is not a meaningful disclosed metric for this business.

Using the March 26, 2026 share price and year-end fundamentals, valuation looks roughly as follows: P/E ~9.1x on 2025 diluted EPS in CAD; P/S ~0.85x on 2025 revenue converted to CAD using the company’s disclosed FX convention; EV/Revenue ~1.2x; and EV/EBITDA ~5.6x using market cap plus year-end debt less cash. Those are approximate analytical calculations, not company-reported metrics.

Historical context is strong. Revenue has risen from US$129.6 million (2021) to US$226.9 million (2022) to US$316.5 million (2023) to US$449.7 million (2024) to US$589.8 million (2025). Net income moved from US$6.6 million to US$15.1 million to US$27.8 million to US$46.4 million to US$59.5 million over the same period. Share count, however, also rose from 34.33 million issued in 2021 to 39.36 million in 2025, with the biggest step-up in 2024 due to the bought-deal financing tied to QuidMarket.

4. What the Company Does

Propel provides online credit products to consumers underserved by traditional financial institutions. Its operating brands include MoneyKey, CreditFresh, Fora Credit, and QuidMarket, and it also offers Lending-as-a-Service capabilities to third-party institutions plus bank-partner products and, more recently, Propel Bank and FreshLine.

The economic model is a mix of owned-balance-sheet lending, participation interests, fee income from bank/partner programs, and LaaS service revenue. That mix matters because it means not all growth is equally capital intensive: LaaS and forward-flow structures can support revenue growth with less balance-sheet usage than direct lending.

5. Why the Story Matters

The story matters because Propel sits at the intersection of three durable themes: underserved consumer demand, migration from storefront/high-friction lending to digital origination, and institutional appetite for specialty-finance assets when underwriting is strong. Management is explicitly targeting growth via product expansion, new geographies, bank partnerships, UK scaling, Propel Bank, Column/FreshLine, and further AI-enabled efficiency.

It also matters because the public market now has a live contrast case. goeasy’s March 2026 disclosures showed how fast sentiment can collapse when credit quality, reporting integrity, or funding flexibility come into question. Relative to that backdrop, Propel’s messaging around tighter underwriting, improving late-Q4 credit, and new third-party capital commitments becomes more valuable if the numbers validate it in 2026.

6. Revenue Quality Assessment

Revenue quality is above average for the sector, but not elite. The positives are clear: 2025 revenue grew 31%, average combined balances grew 32%, and LaaS service fees grew 191% to US$18.0 million, giving Propel a larger stream of fee revenue that is less balance-sheet intensive than direct lending. QuidMarket also added a new geography and another growth vector.

The main caution is that the business is still fundamentally credit-driven, not SaaS-like recurring revenue. Revenue is linked to outstanding balances, product mix, yields, and credit performance. Annualized revenue yield was 113% in 2025, down slightly from 114% in 2024, while Q4 yield fell to 109% from 113%. That suggests mix is shifting somewhat toward lower-yielding or differently structured products, which is not necessarily bad if it comes with better credit and larger addressable volume.

Cash conversion remains the biggest quality question. Despite positive net income and adjusted EBITDA, net cash used in operating activities was US$25.5 million in 2025 because loan growth consumes cash. Management argues that reclassifying net additions of loans and advances would give a better operating view; analytically that is fair, but from an equity holder’s standpoint the business still requires external funding to scale.

Customer concentration is not disclosed as a major issue. The more relevant concentration risk is funding/partner concentration through bank partners, forward-flow buyers, and institutional funding relationships. That is a real risk even if end-borrower concentration is diffuse.

7. Balance Sheet Risk & Financing Pressure

Balance-sheet risk is manageable, but central to the thesis. At December 31, 2025 Propel had US$23.9 million of cash, US$50.0 million of restricted cash, and US$329.6 million of credit facilities plus US$9.4 million of lease liabilities. Shareholders’ equity was US$261.2 million.

This is not a distressed balance sheet, but it is also not a self-funding lender with abundant excess liquidity. The business model depends on continued access to warehouse/facility capital and institutional forward-flow partners. That is why the February and March 2026 announcements matter so much: the US$60 million Mesirow commitment and additional commitment of up to US$150 million tied to FreshLine are not just “news flow,” they are evidence that the capital markets still trust Propel’s underwriting and servicing platform.

The positive offset is that Propel reduced funding costs in April 2025 by upsizing the CreditFresh facility to US$400 million, refinancing the MoneyKey facility, and lowering weighted average cost of capital by roughly 150 bps assuming full utilization.

Likelihood of a near-term equity raise appears moderate to low based on currently disclosed information. 2025 did bring dilution from the QuidMarket-related financing, but since then management has emphasized debt/funding diversification, forward-flow structures, and even NCIB activity rather than equity issuance.

8. Latest Earnings Review

Q4 2025 was a classic “good growth, bad margin” quarter. Revenue increased 21% to US$155.8 million, loans and advances receivable increased 23% to US$459.8 million, and ending combined balances increased 23% to US$589.5 million. But net income fell 49% to US$5.9 million, net margin dropped to 4% from 9%, adjusted net income fell 53%, and adjusted EBITDA fell 32% to US$21.6 million.

For the full year, the picture was much better: revenue rose 31% to US$589.8 million, adjusted EBITDA rose 7% to US$130.3 million, and net income rose 28% to US$59.5 million. So the issue is not that 2025 was weak overall; the issue is that the exit rate on profitability was weaker than investors wanted.

Provision for loan losses and other liabilities was US$296.9 million in 2025 versus US$222.5 million in 2024, and Q4 net charge-offs as a percentage of average combined balances rose to 14% from 13%. That is the core reason the market was uneasy.

9. Did the Quarter Show Improvement?

Partly, but not cleanly. Credit indicators showed some signs of stabilization by late Q4, and management said delinquency trends improved as underwriting tightening implemented in Q3 and early Q4 began to work through the portfolio. That supports the idea that Q4 may have been the trough in margin pressure.

However, reported quarter-on-quarter improvement in economic quality is not yet proven. Q4 still showed higher realized losses, lower revenue yield, lower net margin, and weaker adjusted EBITDA margin. So the real answer is: the quarter may have set up improvement, but it did not itself demonstrate broad-based improvement in the income statement.

10. Management Commentary Check

Management’s main narrative is that it stayed tight on underwriting, credit improved late in Q4, then it accelerated originations in December, which caused upfront provisioning and marketing costs to hit Q4 while the revenue will be earned later. The numbers broadly support that story. Revenue was only at the low end of the 2025 target range, but ending balances outperformed the updated target, implying a lot of the growth arrived late.

At the same time, management did not fully hit profitability targets. Actual 2025 adjusted EBITDA margin was 22%, below the updated 23%–25% target; net income margin was 10%, below the 10.5%–14.5% initial target; adjusted return on equity was 27%, below the updated 29%+ target. So management’s tone on the long-term opportunity may still be justified, but 2025 was not a clean beat year.

My read: management commentary is credible but self-serving. The explanation fits the data, yet it still amounts to “trust us, the costs came first and the revenue comes later.” Investors should require proof over the next two quarters.

11. Management Credibility Track Record

Management’s track record is good, but no longer flawless. In 2024 the company achieved or exceeded most targets, including revenue growth, adjusted EBITDA margin, net income margin, and returns.

In 2025, performance was mixed. Propel outperformed its updated ending-balance growth target and hit the low end of revenue guidance, but fell short on profitability and return metrics. That does not destroy credibility, but it does downgrade the story from “consistent executor” to “credible management navigating a tougher credit year.”

There is also a positive credibility point relative to sector peers: unlike the recent goeasy situation, Propel has not disclosed historical reporting corrections, covenant waivers, or funding-line concessions tied to sudden charge-off shocks. In the current environment, that relative stability matters.

12. Key Positives

Propel has built a very strong multi-year growth record, with 2025 revenue up 31% and ending balances up 23% despite tighter underwriting.

It has broadened the model beyond pure on-balance-sheet lending through LaaS, bank partnerships, forward-flow structures, and FreshLine/Column. That should support faster growth with better capital efficiency over time.

Institutional capital still appears available to Propel. The Mesirow and additional FreshLine commitments are meaningful votes of confidence.

Insider alignment is strong, with directors and executives collectively owning 35.91% of common shares.

13. Key Concerns

Earnings quality is not as strong as headline adjusted metrics suggest. Full-year adjusted EBITDA was US$130.3 million, but operating cash flow was negative US$25.5 million because loan growth consumes cash.

Q4 2025 margins weakened sharply. Net income margin dropped to 4% and adjusted EBITDA margin to roughly 14% in the quarter, versus much stronger prior-year levels.

Provisioning and credit remain the swing factors. Net charge-offs rose, and the allowance for credit losses remains one of the key audit matters given the judgment involved.

The business remains dependent on external funding markets and partner structures. That is normal for this model, but it is a real risk if investor appetite or warehouse conditions tighten.

14. Inflection Point Assessment

Yes, potentially — but the evidence is incomplete. The likely inflection is that underwriting tightened during 2025, credit improved by late Q4, and new product/funding channels are launching into 2026. The company’s 2026 targets imply meaningful re-acceleration in both revenue and profit.

The problem is that inflections in subprime lending can be faked by timing. A strong ending-balance number can coexist with weak near-term profitability and weak cash conversion. So the inflection is possible, not proven.

15. SWOT Analysis

Strengths: strong revenue CAGR, diversified product/funding model, high insider alignment, proven digital underwriting/servicing platform, growing fee-based LaaS component.

Weaknesses: earnings quality only mixed, funding dependence, complex accounting around ECL and adjustments, sensitivity to credit performance.

Opportunities: FreshLine rollout, Column partnership, Propel Bank, UK scaling, more forward-flow capital, more LaaS states/partners.

Threats: regulatory “true lender” challenges, macro deterioration, funding market tightening, adverse credit turns, sector de-rating after goeasy’s issues.

16. Catalysts & Timeline

Over the next 6–18 months, the main catalysts are: evidence that Q1/Q2 2026 margins recover from the weak Q4 exit rate; FreshLine scaling nationally with the new capital commitments; visible contribution from Column and Propel Bank; continued LaaS growth; and proof that UK/QuidMarket integration is additive rather than distracting.

A softer but still relevant catalyst is relative valuation re-rating if Propel can demonstrate stable credit while peers remain under pressure. The recent goeasy disruption creates an opening for that.

17. Variant View / What Could Prove This Thesis Wrong

The thesis is wrong if Q4 2025 was not timing-related but instead the first sign of a structurally worse credit book. In that scenario, 2026 revenue could still grow while provision expense, net charge-offs, and acquisition costs keep margins depressed.

It is also wrong if FreshLine, Column, or Propel Bank scale slower than expected, or if third-party capital becomes more selective. This is especially important because the 2026 plan assumes strategic initiatives launch well without needing new acquisitions.

A final variant risk is regulatory or legal disruption in bank-partner structures. That is a known risk in the AIF.

18. What Investors Should Watch Next

Watch Q1 and Q2 2026 for four things: whether net charge-offs and provision ratios improve; whether Q4’s weak margin was truly temporary; whether revenue converts into better cash generation; and whether new funding/product partnerships produce revenue without excessive upfront cost drag.

More specifically, I would watch revenue versus the US$725–775 million 2026 target, adjusted EBITDA versus the US$152.5–177.5 million target, and whether return metrics actually move back toward management’s goals.

19. Microcap Investment Quality Scorecard

Business Model Quality: 8/10. Strong digital lending platform with multiple brands, geographies, and partner structures.

Revenue Growth Quality: 7/10. Growth is strong and increasingly diversified, but still credit/funding-dependent.

Margin Profile: 6/10. Full-year margins remain solid, but Q4 deterioration was meaningful.

Balance Sheet Strength: 6/10. Adequate, but not fortress-like; external funding remains essential.

Dilution Risk: 6/10. Manageable now, but 2024 showed equity can be used for strategic expansion.

Management Credibility: 7/10. Good long-term execution, mixed 2025 target delivery.

Catalysts & Strategic Positioning: 8/10. FreshLine, Column, Propel Bank, UK, LaaS.

Valuation vs Opportunity: 8/10. Current multiples look modest if 2026 recovery lands.

Composite: 7.0/10. Good microcap/small-cap quality, but not a no-brainer because credit and cash-conversion risk remain real.

20. Microcap Red Flag Detector

Dilution patterns: Possible Concern. Share count rose materially in 2024 for QuidMarket financing, though 2025 dilution was modest.

Promotional management behavior: None Detected from the primary materials reviewed. Disclosure is detailed and target misses are explicitly acknowledged.

Revenue growth with deteriorating margins: Significant Concern in the latest quarter. That is the core issue in Q4 2025.

Declining cash despite growth: Possible Concern. Cash was modest, and operating cash flow remained negative due to loan growth.

Weak cash conversion relative to EBITDA / adjusted EBITDA: Significant Concern. Adjusted EBITDA was positive and growing, but operating cash flow remained negative.

Customer concentration: None Detected / Data limited. No major end-customer concentration disclosure found.

Related-party transactions: None Detected in reviewed materials.

Aggressive adjusted metrics: Possible Concern. Adjusted EBITDA adds back Stage 1 ECL and certain guarantee liabilities; the rationale is understandable, but these are economically relevant in a lender.

Weak disclosure: None Detected. Disclosure quality is relatively strong for a company of this size.

21. Microcap Multi-Bagger Probability Framework

TAM vs current size: favorable. Propel is still small relative to the underserved credit markets it serves in the U.S., Canada, and now the UK.

Scalability: good. The platform supports multiple brands, bank partnerships, and LaaS structures.

Accelerating growth: mixed. Full-year growth is strong, but Q4 profitability decelerated.

Operating leverage: real over time, but not visible in Q4 2025.

Insider alignment: strong.

Differentiation: meaningful, through underwriting/AI, distribution, and flexible funding structures.

Early market penetration: still early enough to matter, especially with new geographies/products.

Overall classification: Moderate Multi-Bagger Potential. The upside path exists, but it depends on maintaining credit discipline while scaling. This is not a software multiple story; it is a specialty-finance execution story.

22. Final Analyst Take

Final call: constructive, but selective.

Propel still looks like one of the better-run public names in underserved consumer fintech. The company has real scale now, strong multi-year revenue growth, high insider ownership, improving product breadth, and fresh evidence that external capital partners remain willing to fund new initiatives. Relative to what just happened at goeasy, Propel currently looks like the steadier operator.

That said, the latest quarter was not clean, and investors should not dismiss that. The 2025 report showed mixed quality of earnings: net income and adjusted EBITDA were positive, but adjusted metrics benefited from credit-loss-related add-backs, while operating cash flow stayed negative because growth consumed cash. In other words, the business appears profitable, but not fully self-funding in the way a casual glance at adjusted EBITDA might imply.

My judgment is that Propel deserves a positive bias only if you believe Q4 2025 was a transition quarter rather than the start of a worse credit cycle. The evidence so far leans in management’s favor, but not decisively. I would describe the stock today as promising, undervalued on normalized 2026 numbers, and still carrying real credit/funding execution risk.

23. Mock Investment Strategy (Conceptual)

Conceptual only, not investment advice.

OPINION: The stock looks inexpensive enough that a margin-recovery confirmation could drive a meaningful rerating, but the market is unlikely to fully reward 2026 targets until it sees at least one or two clean quarters. Current valuation already reflects skepticism.

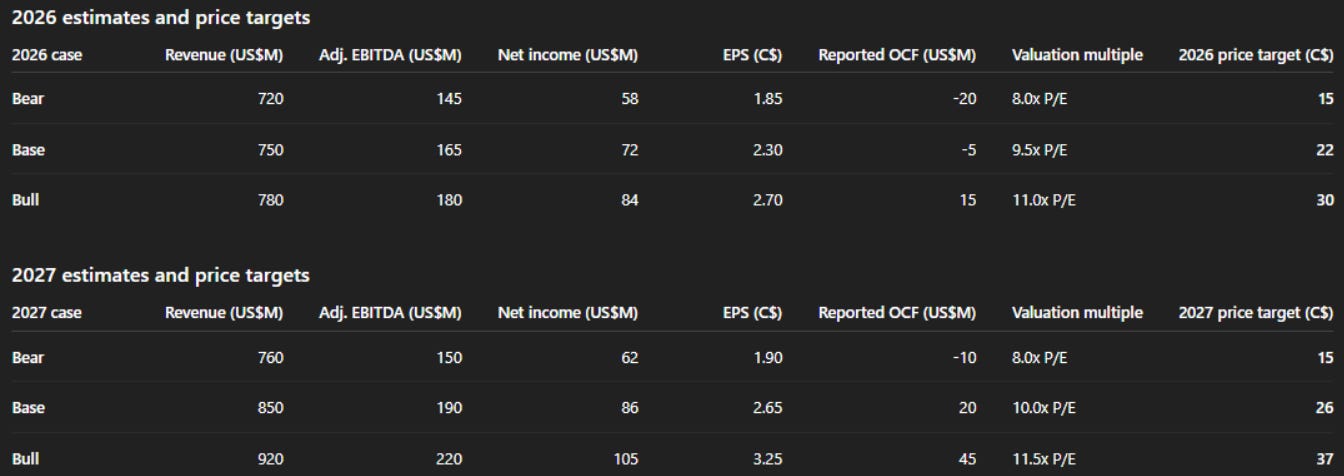

My base case is C$22 for 2026 and C$26 for 2027.

What has to happen for that to work:

2026 lands roughly around the middle of management’s revenue and EBITDA target range.,

Q4 2025 turns out to be a timing/provisioning issue, not the start of a structurally worse credit book.,

FreshLine / Column / new capital commitments support growth without a big new margin reset. Propel announced FreshLine plus an additional commitment of up to US$150 million, on top of the earlier US$60 million Mesirow forward-flow commitment.,

Why I am not using a higher multiple:

Propel is still in a sector where the market is paying close attention to credit quality and funding durability.,

The recent goeasy disruption likely makes investors less willing to pay up until Propel proves margin recovery with real results. That is a relative positive for Propel if it executes, but a valuation cap until then.,

My practical framing:

Below ~C$16: the market is pricing in something closer to a structural credit problem.,

Around C$22: fair value if 2026 is a decent but not spectacular recovery year.,

Above C$30: you need clean credit, strong FreshLine scaling, and convincing 2027 self-funding progress.

Looking at the risk vs. reward profile for 2026:

Bear case is a 15% drop in share price (minus the dividend) so closer to ~10% loss risk. Plus a chance at recovery in 2027.,

Base case is a ~25% gain plus the dividend. Using all fairly reasonable numbers in a normal market.

Bull case is probably a 75% gain when you combine price and dividend.

24. Human Opinion

An investor who has researched Propel Holdings more than myself read this report and made the following comment…

I think the upside potential with the relationship with Column and general growth in banking isn’t really considered. Otherwise, pretty reasonable. I still think 10 PE should be the baseline. Which to me is $20 right now, expectations for $25 next year and $30+ the next.

Which tells me the AI is doing exactly what I want (and what I warned about). It’s arguably not factoring in enough forward growth from aspects of the business that are harder to measure (more speculative or human connected) and it’s arguably not tacking on a high enough valuation multiple. It’s being conservative and isn’t just another “I love this stock I’m super bullish” human produced hype article that’s so common on Substack.

This AI report discussed the obvious potential of Propel Holdings, while also pointing out the risks that a bullish human author may not.

25. Sources

Primary materials reviewed:

● Propel Holdings Q4 and FY2025 audited financial statements.

● Propel Holdings Q4 2025 MD&A.

● Propel Holdings FY2024 audited financial statements and Q4 2024 MD&A.

● Propel Holdings FY2023 and FY2022 audited financial statements; FY2021 year-end financial statements.

● Propel Holdings 2024 Annual Information Form.

● Propel Holdings March 2, 2026 earnings release.

● Propel Holdings February 25, 2026 Mesirow/FreshLine funding announcement.

● Propel Holdings March 10, 2026 FreshLine launch and additional US$150 million commitment.

● Propel Holdings April 28, 2025 funding-cost/facility announcement.

● Propel Holdings IR stock/analyst coverage page and TMX quote page.

Recent comparator / sector context:

● goeasy March 10, 2026 operational update.

● goeasy March 24, 2026 amended financing arrangements.

● Reuters reporting on goeasy’s March 2026 charge-offs, covenant relief, facility repricing, and delayed results.

Seriously, this is NOT financial advice.

I mean it. None of this is financial advice—I say it all the time, and I genuinely mean it. I don’t know you. I don’t know your experience level, risk tolerance, debt situation, or anything else about your financial position.

So please - don’t buy, sell, or hold a stock just because of my opinion in this article.

I have been wrong plenty of times, and I strongly encourage everyone to invest within their own capabilities and consult a financial advisor if needed.

Owning a stock can create bias so please be aware of this. At the time of writing this article I own a 2% position in Propel Holdings in my microcap portfolio.

I was not paid (or compensated in any way) for this article from any companies I discussed, or anyone affiliated with the companies discussed in this article.

Thank you! 🙏

100% agree with your take on AI. The main benefit of buying any investor substack at this point would just be to hear about obscure ideas that there’s barely any documentation on. Every time I use deep research I am amazed.

to me this is just 90% repeating the Q4 transcript over and over again in one way or another.

0 ability to assess the business going forward.