Zedge Inc

A Cash Heavy $32M Market Cap Stock w Big Potential

Another USA listed microcap stock for you.

A cash heavy value stock with significant share buybacks, a shiny new 2% dividend, and the potential for growth in 2026 has me interested enough to buy a 1.5% position in my microcap portfolio and will be watching for greater execution in 2026.

Lets get started.

As always this is NOT financial advice. I know nothing about you - especially your investing experience, experience with microcap stocks, or risk tolerance. So this is NOT a solicitation to buy/hold/sell this stock. It’s simply me discussing my opinions, and to help you get started with your own research and making your own decisions.

Zedge Inc - Ticker ZDGE on the NYSE American (a good little US exchange).

Share price: $2.48 USD

Market cap: $32.25M

Cash: $18.6M with $0.5M FCF in Q2-2025.

Debt: No true debt.

Enterprise Value: $13.65M

Implied fully diluted shares: ~13M

Notes: $5M of share buybacks in 2025 and newly introduced ~2% dividend paid quarterly.

The Short Investing Thesis

Zedge makes phone apps, and they have done this with success and producing cash. The problem for Zedge is that artificial intelligence is both a positive and a negative for their business.

The “bull thesis” that got investors excited about Zedge (driving share price up to 52-week highs in July) is that Zedge is using AI to produce ~6 new products every year. If only 1-2 products every year are successful, then Zedge has the cash and experience to market those products to success.

The “bear thesis” with Zedge down 48% from their recent highs - is that they are competing against AI. For example, one of their core products Emojipedia is down 11% in revenue because Google now makes emojis copy-and-paste right from search. A minor change for Google is a problem for Zedge.

So the investing thesis for Zedge has to involve them winning a fight against AI (by using AI) and implementing products with enough personal touch from humans to become success stories. They intend to pay dividends and buybacks from FCF, and shareholders are hoping for growth to send share price higher.

What They Do

This is another one of those interesting companies where you can actually try their products - to see if you like them. I currently have purchased Zedge premium which is a wealth of phone wallpapers and ringtones at a much cheaper price than buying from my Samsung provider. I also have my 12 year old daughter trying out Syncat where she makes videos of our cats for her socials. She likes it so far.

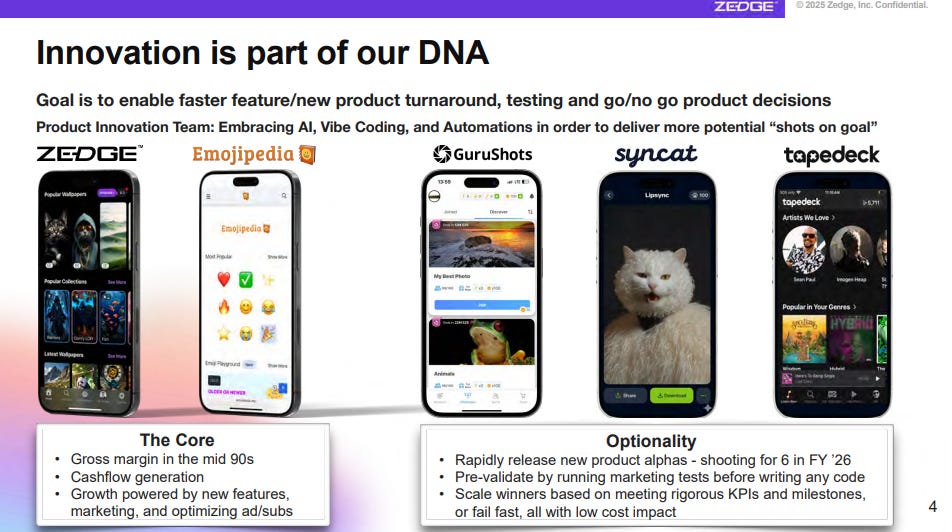

This is a great slide to show both the bull case (and the challenges) of Zedge. Their Zedge core product is doing well, but their “core” product Emojipedia is down 11% that’s not good. They are re-launching GuruShots 2.0, syncat, and tapedeck… and all these products could reasonably fail. I think anyone who produces content (videos, apps, articles, etc.) understand how hit-or-miss these things are. But again it’s more at-bats for the company with a fantastic reward payout (high margins) with low risk (fairly cheap to produce).

So am I introducing Zedge and basically gambling that they find success again. No - not really. There’s two things that Zedge are doing right now that has me a bit more bullish than the market…

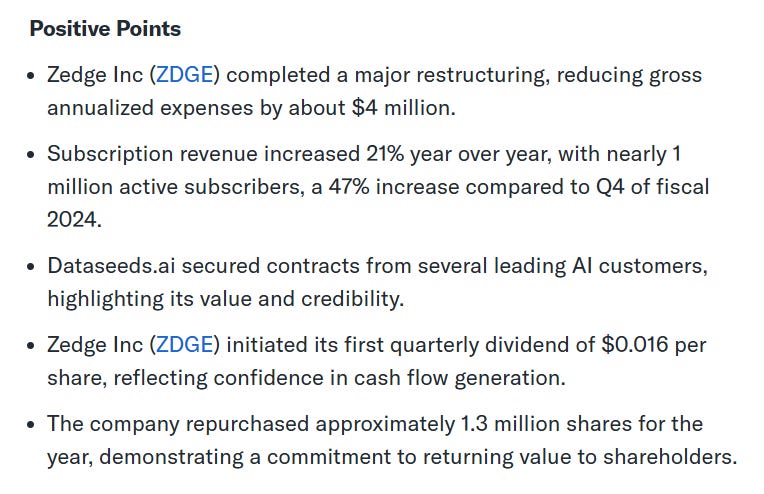

KPI’s and B2B’s

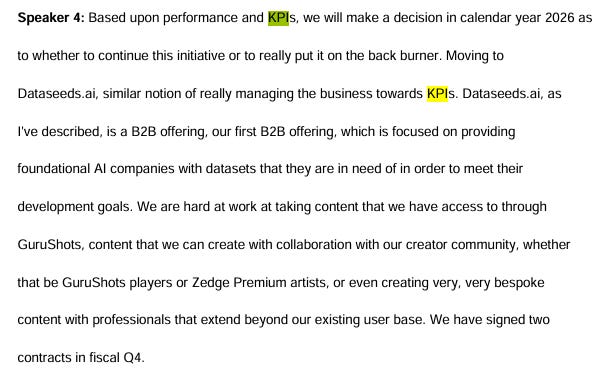

This image is pulled from Zedges Q4 transcript, and it discusses two things.

Everything they do is informed by KPI’s. This management team isn’t guessing. They intend to produce ~6 new products every year, and let the data inform their decisions. I like this!

They are adding a business-to-business revenue vertical in DataSeeds.AI and again it could fail, but at least in Q4-2025 they say they signed two contracts. So this typical B2C company is also adding a potential B2B component. I like this as well!

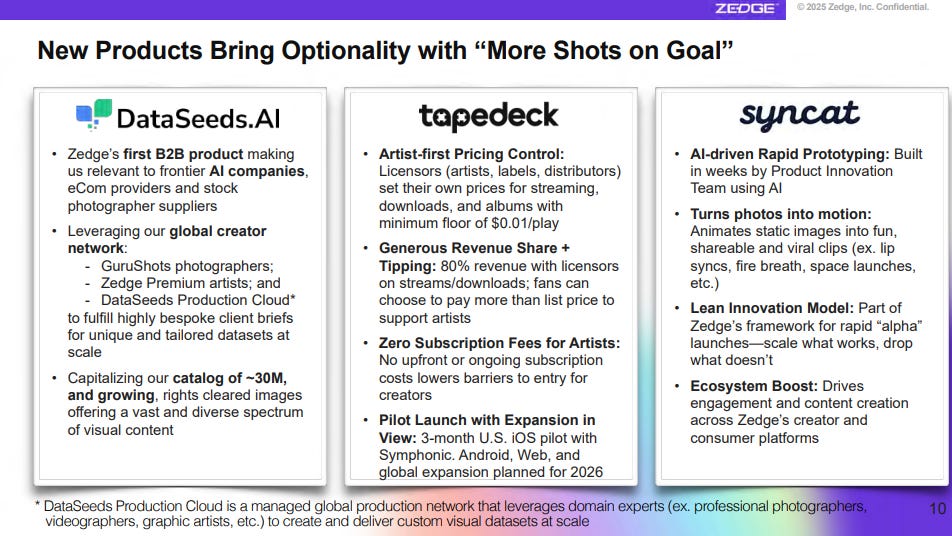

What is DataSeeds.AI ?

For years Zedge has been collecting content from creators. Real humans who produce content use Zedge to monetize their content. Now Zedge has the opportunity to sell that content to artificial intelligence. When you ask AI to give you an image … where do you think AI gets the data from to build your requested image?

So this is quietly a very unique opportunity. Zedge hasn’t really given any expectations for revenue or margins on this product that I’m aware of. Like all of their products, it might fail. However this could be a really good opportunity for a $32M market cap company!

Bull verses Bear Argument?

Let’s start with the bear argument - some challenges with Zedge?

Hard company to model for quant investors. Two products on the decline, at least two products on the incline … maybe more? We don’t know. This adds some volatility and hit-or-miss type revenue growth.

Investors obviously didn’t like the new dividend. Zedge share price was increasing and everyone was happy with the share buybacks. So I have to question how competent management is when they stop going with what was working, and introduce something new that most retail investors don’t want.

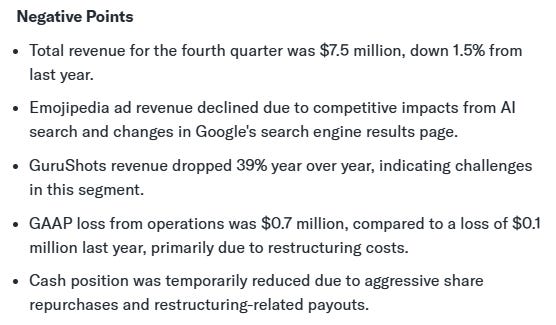

GuruFocus always does a good job of summarizing challenges on earnings, and in the below image they point out the decline in revenue, the decline in their core business Emojipedia, the

destructionrestructuring of GuruShots, and how their cash position took a hit.

So the bear argument for Zedge is that it goes nowhere and does nothing - dead money. They might spend the next 5 years replacing losing products with winning products and never really get ahead. That’s a concern that will limit how long I intend to hold Zedge to give them a reasonable shot at execution.

The Bull Argument - Some Reasons I like Zedge

My “bear argument” is legit - this stock might be dead money. However for a $32M market cap company on the NYSE American it’s also fairly low risk.

~$8M of share buybacks in the past two years.

$18.6M cash and producing FCF even on “weak quarters”.

At a $2.48 share price $1.41 is pure cash.

A stupid 2% dividend 👎

Company intends to fund dividends/ buybacks entirely from operating cash, keeping their $18.6M cash reserve to invest in growth when opportunity arises.

It could be “dead money” - unless they get some growth. Can they get some growth? Moving into the B2B space, and making “data-driven-decisions” gives me some confidence they can. It’s not a guarantee, but I like a company with limited downside risk and multiple shots-on-goal.

All this company really needs is 1-2 winners. Thanks to AI they are able to produce ~6 new products a year, and if the KPI’s say they might have a winning product they have the cash to market the heck out of it. So this is very much a “swing for the fences” hit-or-miss stock. If they can get those 1-2 winning products then Zedge is going to make shareholders money. If they can’t then I will probably be selling in 12 months.

Summary

With a disappointing Q4 out of the way, a 48% drop in share price, and a Q1 expected very quickly on December 15th - I think investors are in ZERO hurry. There is time to do research and make some decisions, maybe even watch what happens on Q1 and see if that helps inform how the rest of 2026 goes. Overall though I like this company. Very much a hit-or-miss if they don’t find success, but if they can produce some successful products it’s at a really interesting price. 57% cash and multiple ways to succeed.

I hope you enjoy the video.

Seriously, this is NOT financial advice.

I mean it. None of this is financial advice—I say it all the time, and I genuinely mean it. I don’t know you. I don’t know your experience level, risk tolerance, debt situation, or anything else about your financial position. So please, don’t buy, sell, or hold a stock just because of my opinion in this article.

I’ve been wrong plenty of times, and I strongly encourage everyone to invest within their own capabilities and consult a financial advisor if needed.

I own a 1.5% position in my microcap portfolio in Zedge stock ZDGE. I was not paid or compensated in any way for this article or video from Zedge or anyone related to Zedge.

Thank you! 🙏

You outlined Zedge’s risk-reward profile with clarity and fairness. I liked how you highlighted their data-driven product approach and new B2B vertical because it shows disciplined experimentation in a volatile niche. According to Nasdaq data, microcaps with net cash exceeding 40% of market cap have outperformed peers by 11% annually over the past decade, validating your focus on downside protection. I wonder whether Zedge’s pivot toward DataSeeds.AI can meaningfully diversify revenues before existing products lose more ground.